5.1 Perpetual Swaps: Overview

TradeView enables fully on-chain perpetual futures trading through deterministic smart contracts, optimized for institutional-grade performance and real-time transparency. The perpetual swap module underpins the trading layer, combining core contract logic with user-defined margin parameters and seamless settlement processes.

5.1.1 Core Design and Settlement Logic

-

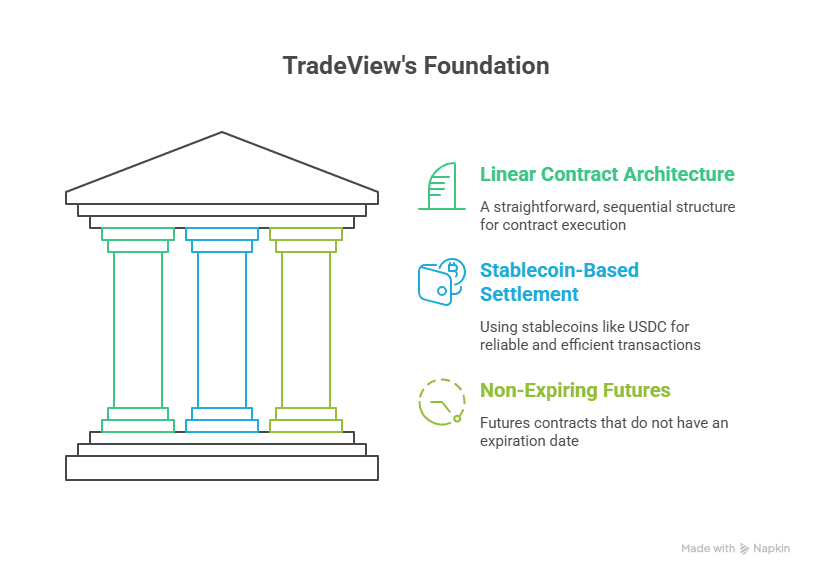

Linear Contract Architecture

-

All perpetual contracts are linear in design, meaning PnL is calculated in USDC rather than in the base asset.

-

Ensures easier accounting, especially for traders managing multi-asset portfolios.

-

-

Stablecoin-Based Settlement (USDC)

-

PnL, collateral deposits, and margin requirements are denominated and settled in USDC.

-

Enables deterministic pricing and avoids volatility exposure in settlement layers.

-

-

Non-Expiring Futures

-

Contracts do not expire, allowing users to maintain directional exposure indefinitely.

-

Eliminates rollover complexities typical in expiring futures markets.

-

5.1.2 Market and Contract Specification

-

Dynamic Market Configuration Per Asset

-

Each listed market (e.g., BTC/USDC, ETH/USDC) has isolated contract specifications:

-

Lot Size: Smallest tradable unit. Example: 0.001 BTC

-

Tick Size: Minimum price increment. Example: $0.10 for ETH

-

Multiplier: Defines the contract size. Typically 1:1 with the underlying asset.

-

Max Leverage: Defined by asset-specific risk tiers and market volatility.

-

-

-

Index Price Calculation

-

Derived from a volume-weighted average of external exchange prices.

-

Sourced from decentralized oracles (e.g., Chainlink, Pyth) to avoid dependency on any single price source.

-

This index is used to:

-

Anchor the funding rate formula

-

Determine liquidation thresholds

-

Compute mark-to-market PnL

-

-

5.1.3 Supported Order Types

-

Primary Order Types

-

Market Orders: Executed immediately against available liquidity at the best price.

-

Limit Orders: Executed at or better than a user-defined price.

-

Stop Orders: Triggered when price crosses a predefined threshold.

-

Conditional Orders: Linked to external variables or price logic (oracle conditions, volatility, block height).

-

-

Advanced Execution Orders (Smart Contract Encoded)

-

TWAP (Time-Weighted Average Price): Breaks large orders into timed intervals to reduce price impact.

-

OCO (One-Cancels-the-Other): Simultaneously sets a stop-loss and take-profit condition.

-

Trailing Stops: Adjusts stop price dynamically as the market moves in favor of the position.

-

Iceberg Orders (Planned): Breaks visible orders into hidden sub-orders to reduce signaling risk.

-

-

Deterministic Execution via Smart Contracts

-

All order types are managed on-chain, without off-chain bots or middle layers.

-

Ensures atomicity, transparency, and auditability of the order lifecycle.

-

5.1.4 Real-Time On-Chain State Tracking

-

Open Interest Monitoring

- Each market maintains a real-time open interest counter to reflect position sizes across long and short participants.

-

Mark Price & PnL Calculation

-

Mark price is derived from the index oracle to minimize manipulation.

-

Unrealized and realized PnL tracked per user position and displayed via APIs/UI.

-

-

Position Lifecycle Management

-

When orders are filled, user positions are created or updated based on:

-

Entry/Exit Price

-

Position Size

-

Leverage & Margin Mode

-

Unrealized PnL and Liquidation Buffer

-

-

5.2 Leverage Support: Up to 50×

TradeView’s architecture enables users to amplify their positions using leverage, empowering capital-efficient trading while embedding on-chain safety mechanisms to manage risk. The leverage system is inspired by high-performance perpetual platforms and tuned for transparent and modular enforcement on-chain.

5.2.1 Leverage Overview and Definitions

-

Leverage Mechanism

-

Allows traders to open positions greater than their collateral balance.

-

Expressed as a multiple of the margin: e.g., 10× leverage means a trader controls a position 10× larger than their posted collateral.

-

Enables both long and short positions with directional exposure.

-

-

Initial vs. Maintenance Margin

-

Initial Margin (IM): Minimum collateral required to open a leveraged position.

- For 50× leverage: IM = 2% of notional value.

-

Maintenance Margin (MM): Minimum margin to keep the position open.

- Typically set at 50% of IM (e.g., 1% for 50×).

-

5.2.2 Margin Calculation and Enforcement

-

Real-Time Margin Ratio Tracking

-

The margin engine constantly evaluates margin health using the formula:

- Margin Ratio = (Equity / Position Notional)

-

Enforced through block-level checks, oracle price updates, or system-triggered events.

-

-

Smart Contract Enforcement

-

All leverage-related thresholds (IM, MM, liquidation buffers) are embedded in TradeView’s on-chain margin contracts.

-

No off-chain risk calculations, ensuring fully deterministic execution.

-

5.2.3 Tiered Leverage System

-

Risk-Adjusted Tiers for Position Sizes

-

TradeView employs a dynamic leverage model to account for market depth and volatility.

-

As position size increases, the max allowable leverage decreases to reduce systemic risk.

-

-

Example: BTC Market Tiers

-

Position ≤ $10K → Up to 50×

-

$10K < Position ≤ $100K → Up to 25×

-

Position > $100K → Max 10×

-

-

Why Tiered Models Matter

-

Protects order book depth and liquidity.

-

Prevents large whales from using max leverage irresponsibly.

-

Ensures fair risk distribution across trader profiles.

-

5.2.4 Market Configuration and Governance Control

-

Leverage Config Per Market

-

Each asset pair can define:

-

Max leverage

-

IM & MM thresholds

-

Position size caps

-

Volatility sensitivity coefficients

-

-

-

Governance-Controlled Parameters

-

These parameters are adjustable via protocol governance.

-

Allows future responsiveness to market volatility, liquidity changes, or systemic events.

-

5.2.5 Trader UX and System Feedback

-

Position Leverage Toggle

-

Users can select the desired leverage via the UI or contract interface at order time.

-

TradeView displays real-time IM/MM ratios, liquidation price, and unrealized PnL.

-

-

Warning and Failsafes

-

Real-time alerts when margin usage exceeds safety thresholds.

-

Contracts reject orders that violate leverage or margin rules.

-

5.2.6 Technical Implementation Details

-

Precision & Rounding

- Margin and PnL values are calculated using fixed-point math (e.g., 18 decimals), ensuring accuracy in low-latency environments.

-

Oracle Integration

-

Leverage limits and liquidation thresholds depend on fast, tamper-resistant oracle feeds.

-

TWAP and spot sources are used to reduce price manipulation risk.

-

-

Gas Cost Optimization

- Margin checks are batched with execution and order placement to minimize computation overhead.

5.3 Isolated vs Cross-Margin

TradeView supports dual margining mechanisms — Isolated Margin and Cross Margin — designed to offer maximum capital flexibility, programmable risk segmentation, and deterministic enforcement at the smart contract level. Unlike centralized exchanges that rely on backend abstractions, TradeView encodes both margin modes on-chain, allowing position-specific margin logic and transparent liquidation flows.

These two modes serve different trader needs and risk profiles and are toggled per-position at execution time.

5.3.1 Isolated Margin: Risk-Segmented Collateralization

Definition and Architecture:

-

Every position in isolated margin mode is assigned a dedicated collateral amount that is not shared with any other position.

-

This margin is escrowed at the time of position creation and remains logically and technically bound to that position.

-

A position-specific vault manages the accounting, PnL, and margin requirements.

Smart Contract Characteristics:

-

Isolated positions instantiate a separate margin sub-account.

-

All balance updates (PnL, funding, liquidation) are scoped to this sub-account only.

-

No implicit collateral credit is given from other positions or system balances.

Risk Management Benefits:

-

Loss containment:

-

Traders can take high-risk directional trades with a predefined loss ceiling.

-

A failed isolated position has no access to other funds in the account.

-

-

Predictable liquidation boundary:

- Easier for vaults or automated bots to forecast risk outcomes.

-

Ideal for strategy isolation:

- Traders deploying different strategies (trend-following, mean-reversion, event-driven) can separate margin pools.

Advanced Use Cases:

-

Multi-strategy automation:

- Vaults running concurrent strategies can keep risk boundaries modular.

-

Quant frameworks:

- An isolated margin is useful for parallel strategy testing with deterministic failover.

-

Third-party bots:

- Enables vault managers or custodial interfaces to allocate fixed budgets per trade or client.

5.3.2 Cross Margin: Shared Equity, Unified Exposure

Definition and Architecture:

-

All positions under cross margin share a single, unified margin pool tied to the account’s equity.

-

Profits and losses across markets are pooled and netted in real-time.

-

On-chain accounting tracks effective margin utilization and available balance dynamically.

Smart Contract Implementation:

-

A master margin vault per account reflects total USDC collateral, unrealized PnL, and funding accruals.

-

When opening a cross-margin position, the system computes effective margin usage across all open positions.

-

Positions draw liquidity on demand from the shared pool, constrained by margin availability.

Capital Efficiency Benefits:

-

Offsetting PnL:

- Profitable positions reduce the effective margin stress of losing ones.

-

Reduced idle capital:

- Users don’t need to overfund each position individually.

-

Auto-rebalancing effect:

- The system reallocates capital to where it’s needed most.

Risks and Limitations:

-

Cascade Risk:

- A major drawdown in one position can trigger liquidation across all cross-margin trades.

-

Volatility sensitivity:

- Requires tighter monitoring and faster Oracle updates.

-

Vault interference:

- Not ideal for multi-user vaults or asset-segregated mandates.

5.3.3 Architectural Comparison: Cross vs. Isolated

| Feature | Isolated Margin | Cross Margin |

|---|---|---|

| Collateral Scope | Position-specific | Account-wide shared collateral |

| Risk Containment | Localized per position | Systemic across all open positions |

| PnL Netting Across Positions | No | Yes |

| Capital Efficiency | Moderate (capital locked per position) | High (capital reused across trades) |

| Margin Accounting Module | Sub-account-based vaults | Unified equity vault |

| Ideal Use Case | Strategy isolation, automation | High-frequency multi-market trading |

| Liquidation Trigger | Position-specific | Account-level margin ratio |

| Funding and Fee Accounting | Per position | Pooled with proportional attribution |

5.3.4 Margin Mode Assignment and Switching Logic

TradeView’s margin architecture is uniquely modular, allowing seamless control over risk posture at the position level. Whether using isolated or cross-margin, the platform ensures all assignments, validations, and state transitions occur deterministically and on-chain.

A.1 Assignment at Order Time

-

Explicit Declaration in Transaction Payload:

-

Margin mode is selected and signed off by the user at the time of trade.

-

Order metadata includes: {margin_mode: "isolated" | "cross"} as a required field.

-

-

Smart Contract Routing:

-

TradeView’s margin router module directs the trade to either the cross-margin engine or an isolated vault smart contract.

-

Each vault instance is tied to the position ID and user ID.

-

-

Gas Optimization:

- The margin selection is processed in the same transaction as the order placement, avoiding redundant state writes.

- Dynamic Switching Support

-

Trade-Linked Switching Constraints:

-

Positions cannot switch margin modes mid-life to preserve accounting integrity.

-

Users must:

-

Close their position voluntarily or wait for it to be liquidated.

-

Submit a new order tagged with a different margin mode.

-

-

-

One-Click Reconfiguration (via UI/Bots):

-

The frontend offers a “Switch Mode” toggle which:

-

Cancels active orders (if any).

-

Closes the position at market.

-

Reopens the same position in the selected margin mode.

-

-

All operations are batched into a single transaction using an execution proxy contract.

-

- Real-Time Sync with Clearing Layer

-

State Tracking Components:

-

Margin Mode Registry: Maps position_id → margin_type.

-

Real-time Equity Calculator: Maintains PnL, net margin, available margin.

-

Risk Threshold Engine: Continuously checks proximity to liquidation threshold.

-

-

Cross-Validator Determinism:

-

All mode toggles and assignments are reflected in block-state deltas.

-

Snapshots are embedded into the state root for verifiability.

-

- Margin Preview Calculations

-

Preview Engine Inputs:

-

Oracle feed prices (min 3-source median).

-

Current leverage, asset volatility tier, and position size.

-

-

Previewed Metrics Before Execution:

-

Liquidation Price Range.

-

Max Allowable Leverage.

-

Initial and Maintenance Margin Levels.

-

Post-trade Available Margin Buffer (if applicable).

-

-

Interface Delivery:

-

REST endpoint /v1/margin-preview

-

WebSocket live preview on the order form.

-

5.3.5 Ecosystem Integration and Vault Support

TradeView’s margin modes are not only trader-facing; they’re programmable primitives for bots, vaults, and protocol-level integrations. This unlocks strategic automation, fund management, and governance-enhanced capital deployment.

- Vault Strategy Builders

-

Composability for DeFi Vaults:

-

Vault builders (e.g., structured product developers or bot creators) can assign isolated or cross-margin logic per strategy.

-

Each vault can:

-

Segregate margin per user.

-

Allocate isolated pools to sub-strategies (e.g., ETH-only long vault).

-

Use cross-margin across correlated positions for hedging strategies.

-

-

-

Risk Mitigation for Multi-User Vaults:

-

Protects capital allocation per user without interdependence of losses.

-

Enables vault operators to build performance isolation guarantees.

-

- API Access for Mode Selection

-

Programmatic Margin Configuration:

-

REST Endpoint: POST /v1/position/create with margin_mode key.

-

WebSocket Real-Time Mode Switching (via PositionClose + Reopen logic).

-

-

Synthetic Isolation Logic:

-

Bots can simulate isolated behavior using capped exposure limits under cross-margin.

-

Ideal for protocol-native market makers or leverage-restricted automation.

-

- Governance-Level Configuration

-

Default Mode by Market or User Class:

-

Governance proposals can:

-

Set the default margin mode for high-volatility assets.

-

Impose isolated-only logic for whitelisted tokens or experimental perps.

-

-

-

Tier-Based Margin Mode Controls:

-

Example:

-

Tier 1 users (verified + high volume): Allowed both modes.

-

Tier 0 users (newcomers): Restricted to isolated until account maturity.

-

-

-

Future-Proofing:

- Modular design allows the addition of hybrid or smart-margin models where portions of the margin are dynamically switched based on real-time VaR (Value at Risk).

Investor Note: What Are Perpetual Swaps — and How Do Leverage & Margin Work? Perpetual swaps are like futures contracts — but without an expiry date. Traders can take long or short positions on an asset (like ETH or BTC), speculating on price movement without owning the underlying coin. Here’s how it works: Perpetuals 101 – Real-World Analogy - Think of it like betting on a stock’s price going up or down — but with borrowed money. - If ETH is at $2,000 and you go long with 10× leverage, you control $20,000 worth of exposure with just $2,000 of your own capital. How Leverage Works - Leverage lets you amplify gains — and losses. - With 10× leverage, a 1% price move = 10% profit or loss on your capital. - Most protocols offer up to 50×, but risk control is critical. What’s Margin? - Margin is the amount you must deposit to open or keep a leveraged position. - Initial margin is the capital needed to open a trade. - Maintenance margin is the minimum needed to keep it open — fall below that, and you're liquidated. What Happens If the Market Moves Against You? - If price drops too far, your margin isn’t enough to cover losses. - The system automatically liquidates your position — meaning it’s closed forcibly to prevent protocol loss. Why TradeView Does It Better - TradeView offers both isolated and cross-margin modes — so users can choose between risk-contained or capital-efficient setups. - Positions are managed on-chain, transparently — no off-chain backdoors, delays, or opaque liquidation triggers. - A built-in risk engine constantly checks margin health and liquidates fairly, without MEV games or frontrunning.

5.4 Liquidation Mechanism

TradeView’s liquidation system is engineered to protect platform solvency, ensure orderly market behavior, and minimize loss contagion. It operates entirely on-chain and integrates deterministic logic for fairness, automation, and real-time enforcement of margin rules.

5.4.1 Real-Time Risk Monitoring

-

*Continuous Margin Checks:* The liquidation engine continuously evaluates all open positions against oracle-fed prices and user margin levels.

-

*Per-Block Validation:* At each block, the system calculates:

-

Maintenance margin ratio per position

-

Account equity vs margin requirement

-

Liquidation eligibility flag

-

-

Oracle-Driven Price Anchoring:

-

Medianized, multi-source oracles prevent manipulation

-

Anchor values drive liquidation thresholds and protect against flash crashes

-

5.4.2 Partial vs Full Liquidation Logic

-

Partial Liquidation Flow:

-

If a position drops below the maintenance margin but still retains value, a partial unwind is attempted.

-

The system reduces position size to bring the margin ratio back within safe thresholds.

-

This conserves user capital while maintaining platform solvency.

-

-

Full Liquidation Flow:

-

If the margin ratio continues to deteriorate or partial liquidation fails, the entire position is closed at the current market price.

-

PnL is immediately realized and netted against the remaining collateral.

-

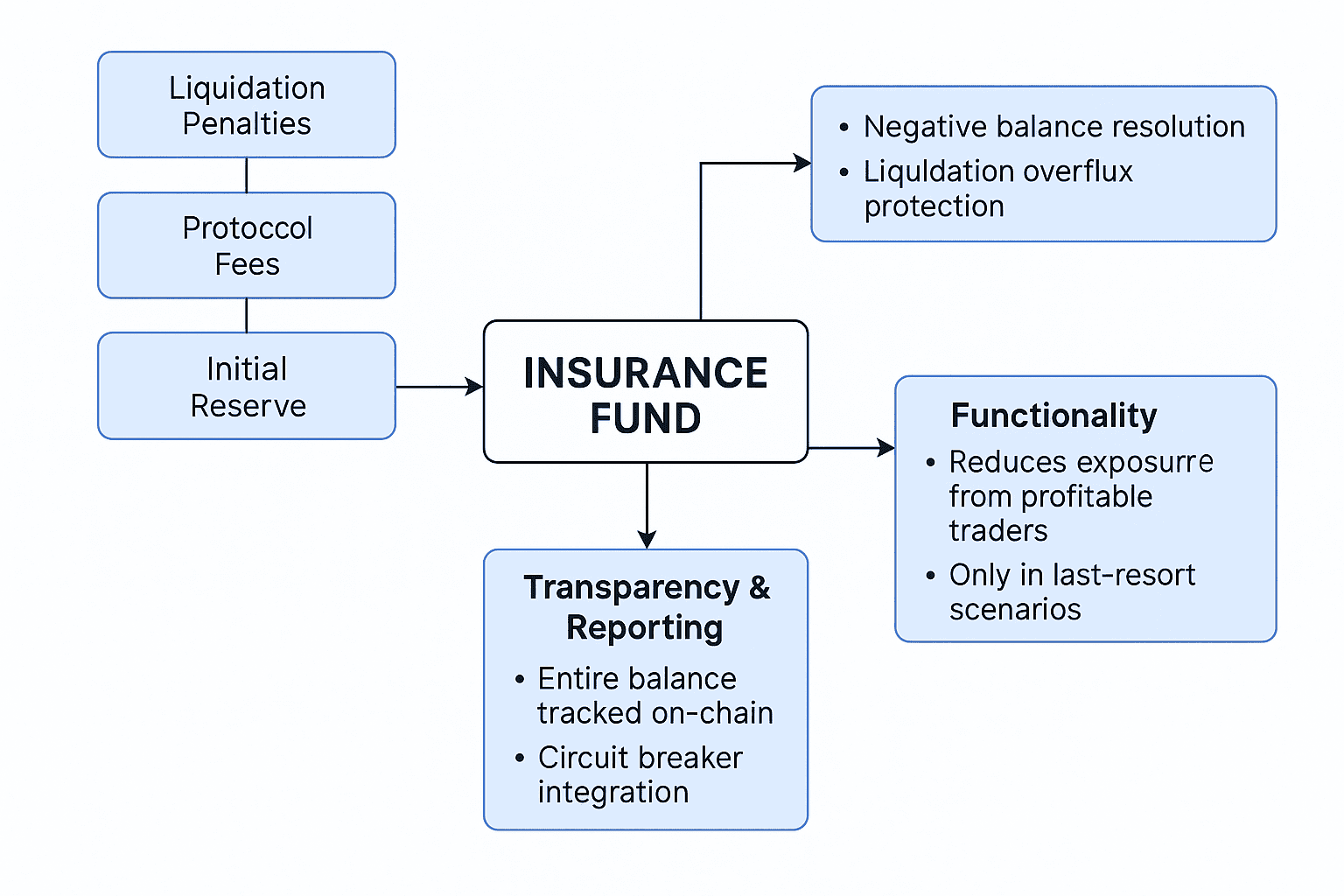

Any excess loss beyond the posted margin is flagged for insurance fund coverage.

-

5.4.3 Architecture of the Liquidation Engine

*Deterministic Liquidation Contracts:* All liquidation paths — whether partial or full — are governed by auditable smart contracts.

-

Inputs: Real-time oracle price, position size, current margin ratio, and maintenance margin threshold.

-

Outputs: Liquidation size, execution penalty, remaining collateral, and insurance trigger (if applicable).

*Auction or Bot-Triggered Execution:* Liquidations are triggered via permissionless on-chain functions. Third-party bots, protocol keepers, or automated vault scripts can initiate a liquidation transaction, ensuring high liveness and decentralization.

-

Execution is trustless and open to anyone with gas.

-

Reverts are prevented via pre-validated liquidation eligibility flags.

*MEV-Aware Liquidation Priority:* To preserve fairness during high-volatility liquidation spikes:

-

TradeView enforces strict FIFO liquidation queues per collateral type, ensuring bots cannot jump the line.

-

Validator reordering is blocked by protocol-layer MEV mitigation rules.

-

Batch liquidation processing is supported to avoid gas wars and ensure equitable opportunity across liquidators.

-

Self-liquidation exploits (where users front-run their own liquidation) are disallowed via signature checks and nonce enforcement.

Visual Only Content

<span class="mark">Content on the left:</span>

-

📉 Oracle Price Update

→ Trigger for real-time margin recalculation -

🧮 Margin Health Check

-

Maintenance margin breached?

-

If yes, flag position for liquidation

-

-

⚖️ Partial Liquidation Attempt

-

Reduce position to restore healthy margin ratio

-

If still under margin → full liquidation triggered

-

-

💥 Full Liquidation Triggered

-

Position closed at market

-

Remaining margin deducted

-

Any loss shortfall sent to Insurance Fund

-

5. Insurance Fund Trigger (Final Node)

-

Covers residual loss if liquidation proceeds fall short

-

Fund replenished via:

-

Protocol fees

-

Liquidation penalties

-

Treasury allocations

-

MEV Protection Layers (On the right side of the graphic)

-

Validator Ordering Control

→ Ensures that liquidation-triggering transactions are processed fairly

→ No front-running by bots or insiders

→ Reordering is blocked at the consensus level -

FIFO Liquidation Queues

→ Liquidation requests queued based on earliest eligibility timestamp

→ Bots cannot outbid each other via gas -

Batch Auction Liquidation* → All eligible liquidations in a block processed at the same penalty curve

→ Prevents last-second sniping or liquidity draining* -

Anti-Self-Liquidation Logic

→ Users cannot trigger liquidations on their own wallet to manipulate insurance coverage or game penalties

—--------------------------------------------------------------------------------------------------------------

*Multi-Collateral Integration:* Each supported collateral asset (e.g., USDC, ETH, LSTs, LP tokens) includes its own liquidation thresholds, haircut ratio, and volatility buffers.

-

Haircut logic and slippage protection are built into the liquidation execution layer.

-

Liquidation logic is extensible to support synthetic assets, derivatives, and cross-chain bridged tokens.

5.4.4 Liquidation Penalty and Incentives

-

Penalty Fee Structure:

-

A penalty (e.g., 2–5% of notional) is charged to the liquidated account.

-

Distributed between:

-

Liquidator or executor

-

Insurance Fund

-

-

-

Dynamic Penalty Curve (Future Roadmap):

-

Larger positions or frequent violations may incur steeper penalties.

-

Encourages responsible leverage usage and discourages toxic behavior.

-

5.4.5 Safety Mechanisms and Cascading Risk Controls

-

Global Circuit Breakers:

- In the event of extreme volatility or oracle malfunction, a protocol-wide halt can be triggered to pause new orders and liquidations temporarily.

-

Risk Parameter Upgrades via Governance:

-

Liquidation ratios, penalties, and trigger intervals can be upgraded by governance proposals.

-

Keeps the risk engine responsive to evolving market conditions.

-

-

Failsafe Backstop:

-

If liquidation fails (e.g., during thin liquidity), the position loss may be covered by:

-

Insurance Fund

-

Auto-Deleveraging (covered in later sections)

-

-

5.4.6 Liquidation Life Cycle (Process Flow)

| Stage | Action |

|---|---|

| Price Feed Update | Oracle updates trigger margin recalculations per account |

| Eligibility Check | Maintenance margin violation is detected for a specific position |

| Partial Liquidation Attempt | The protocol reduces position size to regain compliance |

| Full Liquidation (if needed) | Entire position closed at market; remaining margin realized or forfeited |

| Penalty Distribution | Fees are charged and allocated between the insurance fund and the liquidator |

| Insurance Top-Up (if deficit) | Losses beyond the margin are settled using the insurance fund or the ADL system |

5.4.7 Benefits of TradeView’s Liquidation Architecture

-

Trustless and Transparent:

- All liquidation decisions are executed on-chain, verifiable by any participant.

-

Efficient Capital Retention:

- Partial liquidation avoids unnecessary capital loss and improves user retention.

-

Composability-Friendly:

- Bots, vaults, and protocols can integrate with liquidation triggers to build hedging layers or self-insuring strategies.

-

No Manual Intervention:

- Autonomous execution ensures fairness and eliminates censorship or bias.

Investor Note: What Happens When a Position Gets Liquidated? Liquidation is a safety mechanism to protect the protocol — and other traders — when someone’s position becomes too risky to maintain. Here’s how it plays out: Why Do Liquidations Happen? - You enter a leveraged trade using a small deposit (margin). - If the market moves against you, your losses increase rapidly. - Once your remaining margin can’t cover the loss, the system liquidates (force-closes) your position. Real-Life Analogy - Imagine you put $1,000 down to control a $10,000 bet on ETH. - ETH drops 10%. That’s a $1,000 loss. Your full deposit is gone. - Before this happens, the system intervenes and closes your position to avoid deeper loss. What Makes TradeView’s Liquidation Fairer? - All liquidations are executed on-chain — no centralized middlemen. - A smart contract tracks real-time prices and health ratios. Once a position crosses the liquidation threshold, it gets closed automatically. - Liquidators (other bots or users) are rewarded with a fee for doing this — ensuring fast action. Investor Takeaway Liquidation may sound harsh — but it’s vital for system safety. Without it, one bad position could bankrupt a vault or create bad debt across the protocol. TradeView automates this process fairly, transparently, and with clear protection for both traders and the broader ecosystem.

Here’s a table for what happens when your position goes bad?

| Step | Visual Element | Caption |

|---|---|---|

| 1 | 📥 Entry Icon (e.g., Up Arrow) | User opens leveraged position with initial margin |

| 2 | 📉 Price Down Icon | Market moves against user (e.g., ETH drops by 10%) |

| 3 | 🔴 Red Alert Icon (Meter Half Full) | Margin ratio hits warning zone (risk engine flags position) |

| 4 | 🧮 Calculator Icon + ⚖️ Scale | Liquidation threshold crossed — margin < required maintenance |

| 5 | ⛓️ Smart Contract Icon + 💥 | Position forcibly closed by protocol – liquidator earns penalty fee |

Insurance Fund covers shortfalls. DAO can adjust penalty rules via governance.

5.5 Funding Rate Calculation

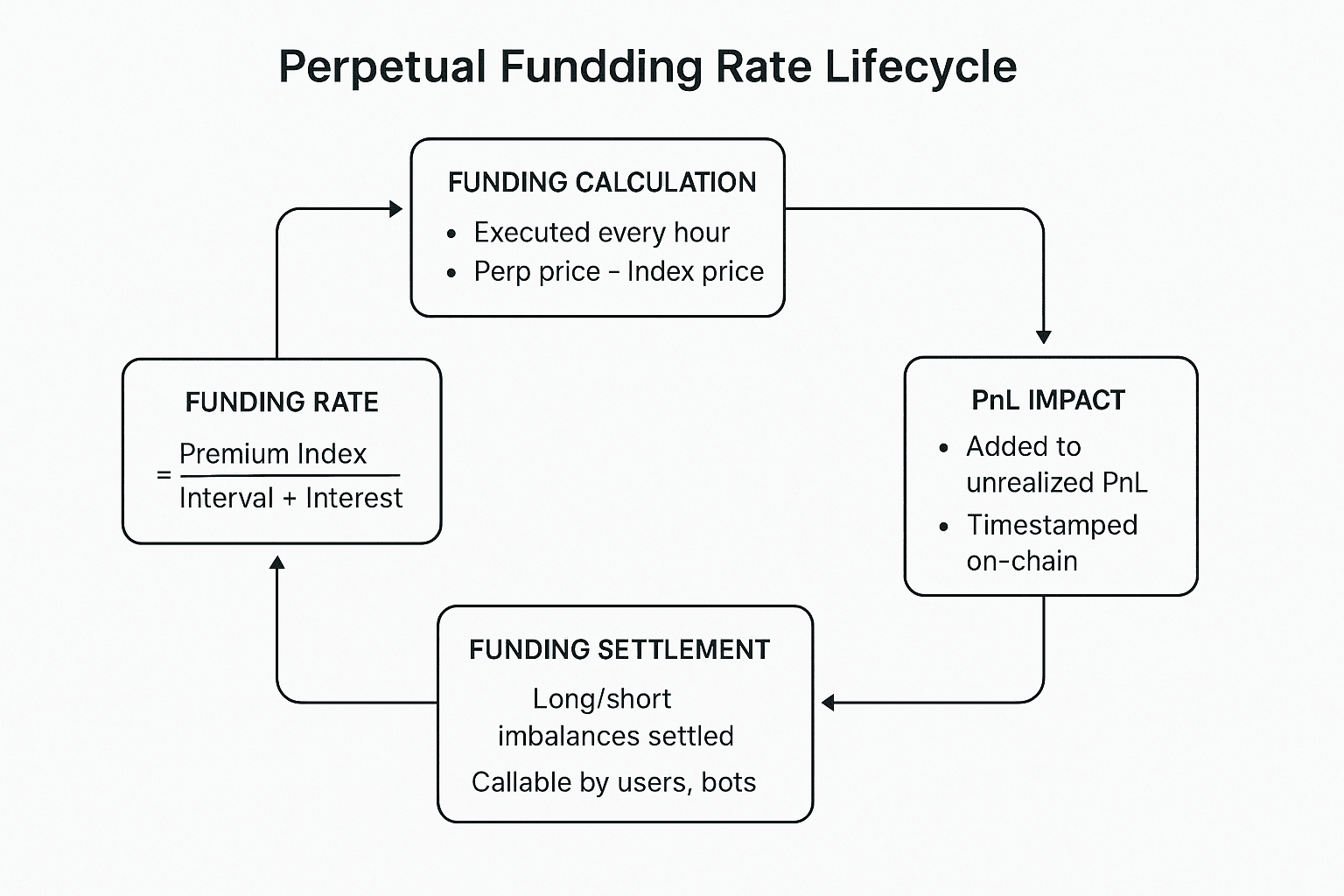

Perpetual futures require a mechanism to keep contract prices aligned with the real-world spot index. TradeView employs a decentralized funding rate system that periodically incentivizes price convergence between the perpetual contract and its underlying index. This mechanism is implemented entirely on-chain and is enforced through deterministic execution logic.

5.5.1 Funding Formula and Pricing Model

-

Purpose of Funding:

-

Encourages price convergence between perpetual swap prices and their corresponding index prices.

-

Ensures that long and short positions are balanced economically over time, preventing prolonged skew.

-

-

Premium Index Derivation:

-

Defined as the difference between the Mark Price (derived from the order book or oracle median) and the Index Price (a time-weighted average from trusted oracles).

-

Expressed as:

Premium Index = (Perpetual Market Price - Oracle Index Price) / Oracle Index Price

-

-

Funding Rate Formula Components:

-

Funding Rate = Premium Index / Anchor Interval + Interest Rate Differential

-

Anchor Interval: Defines how frequently funding recalculations happen (e.g., every hour).

-

Interest Rate Differential: Optional adjustment reflecting the borrowing cost of the underlying vs. the quote asset (commonly used for USDC-settled contracts).

-

-

*Example formula:*

pgsql

CopyEdit

Funding Rate = ((Perp Price - Index Price) / Index Price) / 1hr + InterestRateComponent

-

Rate Clamping and Limits:

-

Maximum funding caps and floors are enforced to prevent extreme values.

-

Example: ±0.75% per funding interval, depending on market volatility.

-

-

Dynamic Recalculation:

-

Executed at defined intervals (hourly by default), with real-time inputs from TradeView’s decentralized oracle network.

-

Uses TWAP (Time-Weighted Average Price) smoothing to prevent manipulation during low liquidity periods.

-

5.5.2 Execution Logic and PnL Integration

-

Automated Hourly Settlements:

-

At the end of every funding interval, long and short traders pay or receive funding payments:

-

If the perpetual is trading above the spot index, longs pay shorts.

-

If the perpetual is trading below the spot index, shorts pay longs.

-

-

-

Impact on Unrealized PnL:

-

Funding payments are integrated into a trader’s unrealized profit/loss and affect:

-

Effective cost basis of open positions

-

Collateral balance available for margin

-

Liquidation thresholds when funding payments push margin ratios below safety limits

-

-

-

Distribution Methodology:

-

Funding is a peer-to-peer transfer — no protocol-level gain or burn.

-

Each position's notional value is multiplied by the funding rate and either credited or debited to/from the account.

-

-

Precision and Atomicity:

-

Payments are settled atomically on-chain to avoid rounding errors or timing disputes.

-

No off-chain computation is involved — each settlement is finalized per block.

-

-

Multiple Markets:

- Each perpetual market maintains its own funding rate, index price feed, and independent settlement ledger.

5.5.3 Triggering, Batching, and On-Chain Synchronization

-

Funding Execution Trigger:

-

Funding calculations and distributions can be initiated by:

-

Any user invoking the funding settlement function

-

Dedicated off-chain bots (keepers) that run scheduled triggers

-

Validator hooks during finalization of a trading block (planned for upgrade)

-

-

-

Gas Incentives for Triggers:

-

Users who execute the funding trigger may receive a gas rebate or reward paid by the protocol treasury.

-

Prevents skipped intervals due to inactivity or high gas volatility.

-

-

Batch Handling Across Markets:

-

A single funding trigger call can settle funding across multiple markets in a batched manner.

-

Designed for performance and cost efficiency when multiple instruments are actively traded.

-

-

Transparency and Auditing:

-

All funding transactions are recorded on-chain with:

-

Funding rate used

-

Timestamp of settlement

-

Amount credited/debited

-

Triggering address

-

-

This ensures that users can independently verify funding histories and cross-check the impact on PnL.

-

5.5.4 Why TradeView’s Funding Model Matters

| Feature | TradeView Implementation | Benefit |

|---|---|---|

| On-Chain Settlement | Fully transparent, irreversible funding transfers | Users trust the system; no hidden adjustments |

| Peer-to-Peer Funding | Longs/shorts pay each other directly | Aligns incentives, no central profit center |

| Oracle-Synced Pricing | Reliable index via decentralized oracles | Minimizes manipulation risks |

| Modular Formula Logic | Funding components can be updated via governance | Flexibility for tuning based on market maturity |

| Open Triggering Mechanism | Any user or bot can call the settlement function | Removes single points of failure and enhances decentralization |

To Conclude TradeView’s funding rate system is robust, flexible, and decentralized by design. It goes beyond just price anchoring — it becomes a mechanism of capital balance, volatility reflection, and PnL truthfulness, all enforced through transparent, autonomous on-chain logic.

5.6 Insurance Fund Logic

The Insurance Fund in TradeView is a core protocol safeguard, designed to absorb unforeseen losses arising from liquidation shortfalls, high-volatility events, or sudden liquidity gaps. Unlike reactive models, TradeView’s fund is proactive, automated, and transparently managed on-chain, aligning economic sustainability with capital protection.

5.6.1 Funding Sources

To maintain resilience, the Insurance Fund draws from multiple revenue-linked and event-driven sources:

-

Liquidation Penalties

-

Every time a position is liquidated, a penalty fee (percentage of notional or remaining margin) is collected.

-

This amount is deposited into the Insurance Fund as compensation for systemic risk.

-

-

Protocol Fee Allocations

-

A fixed share of platform trading fees — especially from the taker side or leveraged trades — is streamed to the fund in real time.

-

This creates passive accumulation during periods of normal market behavior.

-

-

Initial Treasury Reserve

-

At genesis, a portion of the protocol treasury or token allocation is seeded into the fund to ensure it starts solvent.

-

Can be expanded via governance proposals as the platform scales.

-

-

Staking Yield Redirects (Planned)

- In future iterations, staking rewards (e.g., from LST-backed collateral) could be optionally redirected partially into the Insurance Fund.

5.6.2 Functionality

The Insurance Fund is not a passive vault — it actively participates in mitigating liquidation-related debt and supporting platform integrity during stressed market states:

-

Negative Balance Resolution

-

If a user is liquidated and their margin is insufficient to cover losses, the fund absorbs the delta.

-

This avoids default contagion and ensures other traders are unaffected.

-

-

Liquidation Overflow Protection

-

In volatile scenarios, the execution price during forced liquidation might result in larger losses than expected.

-

The fund covers slippage-induced gaps between the maintenance margin and exit price.

-

-

Protocol Solvency Layer

- By acting as a risk buffer, the fund ensures TradeView remains solvent and functional even during tail events.

-

Cascading Liquidation Shield

-

In leveraged environments, one failed position can trigger others.

-

The fund intercepts the chain reaction by reducing net losses before they propagate.

-

5.6.3 Transparency & Reporting

TradeView’s Insurance Fund is engineered with on-chain accountability and auditable logic to ensure trust and decentralized oversight:

-

On-Chain Balance Visibility

- The fund’s USDC balance and contribution sources are published on-chain, accessible to any participant.

-

Automated Smart Contract Access Control

-

Withdrawals, disbursements, and triggers are enforced by immutable smart contracts.

-

No single actor (including admins or validators) can drain or repurpose funds.

-

-

Circuit Breaker Integration

-

If fund balance drops below a critical threshold, emergency parameters (like reduced max leverage or slowed order matching) can be auto-triggered.

-

This protects protocol solvency and gives time for governance to react.

-

-

Periodic Audit Reports (Planned)

- Optionally, third-party or community-verifiable proofs can be attached to ensure correct utilization and fund replenishment pacing.

5.6.4 ADL (Auto-Deleveraging) Backup

In extreme stress events where the Insurance Fund is fully depleted, the system triggers a last-resort safety mechanism:

-

Auto-Deleveraging Mechanism

-

The ADL module begins forcibly reducing the size of profitable traders’ positions on the opposite side of the market.

-

This process is non-preferential, based on a queue system (e.g., highest leverage, highest profit traders are reduced first).

-

-

Loss Sharing Logic

- ADL helps maintain solvency by ensuring the debt is offset by positive P&L positions instead of resulting in unrecoverable losses.

-

Governance-Controlled Thresholds

- ADL activation thresholds and maximum deleverage per trader can be governed over time, adapting to market size and volatility.

-

Failsafe, Not Primary

- ADL is only triggered when the Insurance Fund is zeroed and liquidation at market price is not possible — truly a last-resort fail-safe.