4.1 Layer-1 Blockchain Design

TradeView operates atop a custom-built Layer-1 blockchain, purpose-engineered to support ultra-low-latency, high-throughput perpetual trading at scale. The architecture is designed to optimize determinism, composability, and synchronous on-chain operations — all while preserving decentralization.

4.1.1 Core Design Objectives

-

High-throughput trading environment with deterministic state transitions and no probabilistic forks

-

Sub-second finality to support real-time execution and programmatic risk management

-

Zero-gas trading design with selective subsidization of critical transaction types

-

Composable state layer to support vaults, order logic, and asset accounting natively

-

Validator-managed infrastructure secured via staked consensus and slashing incentives

4.1.2 Modular Infrastructure Components

-

Execution Layer: Built with a Go-based architecture optimized for transaction ordering and EVM-agnostic contract execution.

-

Application Layer: Fully on-chain matching engine, order book, and settlement coordination native to the L1 runtime.

-

Consensus Layer: Tendermint BFT-based consensus providing instant finality and forkless execution.

-

Networking Layer: Uses mempool prioritization logic for liquidation-critical messages and cross-contract syncs.

4.1.3 Native Module Implementations

-

Orders Module: Responsible for lifecycle tracking of advanced and vanilla orders, natively indexable.

-

Accounts Module: Wallet abstraction with internal sub-accounts for multi-asset, cross-margin trading.

-

Risk Engine Module: Evaluates margin, funding, and liquidation criteria on-chain without external dependencies.

-

Collateral Adapter Module: Interfaces with external IBC-like bridges and vaults for multi-chain asset support.

4.1.4 Interoperability and Extensibility

-

IBC-style compatibility for cross-chain asset message ingestion (e.g., from Ethereum, Solana, L2s)

-

Custom APIs and relayer protocols for market data injection, trading bots, and integrations

-

Upgradeable module framework with on-chain governance-controlled upgradability of execution logic.

TL;DR — What This Means for You as an Investor TradeView isn't just another app built on someone else's blockchain. It is the blockchain — one built specifically for high-frequency, real-time trading with no gas fees, no slowdowns, and no reliance on Ethereum’s bottlenecks. Think of it like owning the high-speed rails instead of renting tracks from a congested metro. Here’s the upside: - Sub-second execution means no delays in trade settlement — crucial for pro traders, vault managers, and automated strategies. - Everything lives natively on-chain: the order book, the matching engine, the risk module — not bolted on as an afterthought. - Fully composable: third parties can build vaults, bots, and new products directly into the L1 without latency tradeoffs. - Cross-chain ready: it plugs into Ethereum, Solana, and other ecosystems via built-in IBC-style adapters — making it future-proof and integration-friendly. - Investor peace of mind: validator-based slashing, instant finality, and transparent upgrades reduce forks, MEV chaos, and governance risk. In short: TradeView’s L1 is purpose-built trading infrastructure that you can own a piece of — one that combines the reliability of traditional exchanges with the decentralization of DeFi. If you’ve been burned by gas spikes, stuck orders, or DEXs that buckle under load… this section is why TradeView won’t.

4.2 Consensus Protocol: Tendermint BFT

TradeView’s Layer-1 blockchain achieves deterministic finality and high availability through Tendermint BFT (Byzantine Fault Tolerance) — a battle-tested consensus engine optimized for low-latency transaction propagation and rapid block confirmation. This section outlines how Tendermint operates as the backbone of TradeView’s technical architecture.

4.2.1 Tendermint Overview: Why It Was Chosen

-

Byzantine Fault Tolerance (BFT):

-

Supports fault-tolerant operation even if up to 1/3 of validators behave maliciously.

-

Ensures network security in adversarial conditions without requiring energy-intensive mining.

-

-

Deterministic Finality:

-

Blocks are finalized instantly — no probabilistic confirmations like Ethereum or Bitcoin.

-

Eliminates chain reorgs and rollback risks that break order consistency for traders.

-

-

High Throughput Compatibility:

-

Proven in the Cosmos ecosystem for processing thousands of transactions per second (TPS).

-

Ideal for latency-sensitive systems like perpetual trading platforms.

-

4.2.2 Consensus Flow in Tendermint (TradeView-specific Customizations)

-

Round-based Voting System:

-

Block proposals are made by a rotating proposer validator.

-

Validators go through Pre-Vote → Pre-Commit → Commit phases before a block is finalized.

-

-

TradeView Customizations:

-

Custom block intervals are fine-tuned for sub-second latency on the trading engine.

-

Integration with Oracle update windows and order book synchronization events.

-

-

Vote Signing & Gossip Protocol:

-

All votes are cryptographically signed and propagated over a p2p gossip layer.

-

Ensures block consensus is both secure and globally visible to all nodes quickly.

-

4.2.3 Validator Set & Staking Mechanism

-

Initial Validator Composition:

-

TradeView bootstraps with a permissioned validator set (minimum 16), operated by stakeholders.

-

Over time, transitions to decentralized validator onboarding through staking contracts.

-

-

Validator Duties:

-

Proposing and voting on blocks.

-

Executing order book state transitions and trade settlements.

-

Running relayer modules for cross-chain proof verification.

-

-

Delegated Staking Architecture:

-

Token holders can delegate TradeView's Native Token to validators and earn proportional rewards.

-

Encourages decentralization and long-tail validator participation.

-

-

Slashing & Misbehavior Detection:

-

Misconduct like double-signing, downtime, or equivocation results in token slashing.

-

Real-time validator monitoring is embedded into the chain’s telemetry and governance stack.

-

4.2.4 Network Performance Characteristics Enabled by Tendermint

-

Sub-second Finality:

-

Block times targeted at ~400–600ms for seamless UX in trading environments.

-

Vital for limit order placement, liquidation monitoring, and programmatic trading.

-

-

Liveness under Adversity:

-

With up to 1/3 Byzantine tolerance, the network continues even under attack scenarios.

-

Ensures zero downtime during validator rotation, latency spikes, or partial network partition.

-

-

Synchronized Execution Pipelines:

-

Trade execution, funding rate updates, oracle synchronization, and position recalculations all share a synchronized execution cycle.

-

Guarantees atomic, state-consistent updates across the entire trading stack.

-

4.2.5 Integration with Trading Logic and Smart Contracts

-

State Machine Execution:

-

TradeView’s trading engine logic runs on top of the Tendermint ABCI (Application Blockchain Interface).

-

Clean separation between consensus and application logic for upgrade flexibility.

-

-

Order Matching Interlocks:

- Consensus timing is tightly coupled with order book updates and match engine logic, ensuring deterministic and censorship-resistant trading.

-

Validator-driven On-chain Governance:

- Changes to margin requirements, supported markets, or fee rates can be approved via governance proposals and executed by validator consensus.

4.2.6 Upgradeability and Protocol Evolution

-

Hot-swappable Application Logic:

- Via ABCI, application layer upgrades (e.g., adding new order types or collateral types) do not require hard forks.

-

Governance-proposed Network Upgrades:

- Token holders vote to approve upgrades, and validators coordinate their rollouts securely.

-

Versioned Protocol States:

- Tendermint supports version tagging of state transitions to ensure backward compatibility and seamless node restarts.

Outcome: Consensus Built for Trading-Centric Blockchains Tendermint BFT is not merely a consensus layer — it’s the real-time coordination engine that ensures TradeView’s L1 remains fast, final, and fault-tolerant. By combining performance-grade finality with rigorous validator economics, TradeView guarantees a secure, fair, and seamless experience for traders, institutions, and automated systems.

4.3 On-Chain Order Book Architecture

The on-chain order book is the backbone of TradeView’s decentralized trading infrastructure. Unlike off-chain or hybrid models that rely on third-party relayers or centralized servers, TradeView’s order book is fully embedded within the Layer-1 blockchain. This ensures transparency, atomicity, and composability, without sacrificing performance.

4.3.1 Architectural Design

-

Fully On-Chain State Representation

-

Every order — including price, size, timestamp, and order type — is stored as a state object on-chain.

-

The state transitions (e.g., creation, modification, cancellation) are handled via smart contracts and executed deterministically by validators.

-

This creates a provable, tamper-resistant ledger of market activity.

-

-

Key-Value Store Optimization

-

Orders are stored in a Merkleized key-value map indexed by market ID, price level, and user address.

-

Enables efficient lookups and partial state proofs for lightweight clients and stateless order routing bots.

-

-

Per-Market State Shards

-

Each trading pair (e.g., BTC/USDC) is deployed as an isolated contract shard, reducing inter-market contention.

-

Orders are stored in memory-efficient ring buffers and sorted binary trees to allow fast price-level aggregation.

-

4.3.2 Data Structure Breakdown

-

Order Object Structure

-

orderID: Unique identifier (hash of user address, timestamp, and nonce).

-

marketID: Reference to the instrument or perpetual pair.

-

price: 64-bit fixed-point representation.

-

quantity: Signed integer (positive for buy, negative for sell).

-

timestamp: Block time at placement.

-

orderType: Enum (limit, market, conditional, etc.).

-

status: Enum (active, filled, cancelled, expired).

-

conditions: Optional logic for advanced orders (TWAP, OCO, etc.).

-

-

Order Tree (Price Bucket)

-

AVL/Red-Black Tree per market-side for fast best-price lookup.

-

Each price node stores aggregated quantity and a linked list of order IDs (FIFO per level for fairness).

-

4.3.3 Functional Capabilities

-

Deterministic Sorting

-

Orders are always matched based on strict price-time priority, validated by consensus nodes.

-

Guarantees MEV-resistance and fair execution even under congestion.

-

-

Batch Processing Engine

-

Blocks can process multiple order placements, cancellations, and modifications atomically.

-

Reduces gas overhead and ensures temporal accuracy of bulk trades or bot strategies.

-

-

Gas Abstraction

-

Orders can be submitted via relayers with meta-transaction support, offloading gas fees from end-users.

-

Signature-based pre-verification ensures replay protection and trustless relaying.

-

4.3.4 Smart Contract Modularity

-

Market Factory Contracts

-

Deploys new trading pairs with their order books.

-

Permissioned by governance or dynamically instantiated through proposals.

-

-

Order Management Module

-

Handles CRUD operations for orders.

-

Emits granular events for off-chain indexers and analytics.

-

-

Matching Isolation

- Matching is separated from order maintenance, enabling asynchronous execution logic and modular upgrades.

4.3.5 Security and Finality Features

-

Merkle Commitments

-

Each block includes a root hash of all order book states.

-

Enables zero-knowledge proof integration or partial state verification for external rollup syncs.

-

-

Slashing-Condition Hooks

- If any validator proposes an invalid order state transition (e.g., front-running or double-execution), it triggers slashing based on Tendermint’s consensus.

-

Replay and DOS Protection

-

Nonces and expiration fields prevent reordering or spamming.

-

Per-account rate limits and order lifetime enforcement help mitigate denial-of-service vectors.

-

4.3.6 Composability and API Access

-

On-Chain Queryable APIs

-

Read-only functions expose current top-of-book, market depth, and recent order history.

-

Facilitates integration with bots, aggregators, and strategy vaults.

-

-

Cross-Module Integration

-

The order book state can be composed with:

-

Vaults: For programmatic trading.

-

Risk Engine: For margin and exposure recalculations.

-

Oracles: For volatility-dependent order types like conditional triggers or trailing stops.

-

-

4.3.7 Performance Considerations

-

Memory-Efficient Storage

-

Uses compressed byte-packing and removal of expired orders per block.

-

Minimizes gas and storage bloat without sacrificing order granularity.

-

-

Indexing Layer (Off-chain Augmentation)

-

Optional full-node indexers listen to event logs and reconstruct the order book in real-time.

-

Supports UI responsiveness and historical analysis without burdening on-chain execution.

-

-

Latency Optimizations

-

Block-level batching reduces state write contention.

-

Native matching hints are passed during placement to speed up execution pathfinding.

-

Why It Matters

-

Establishes transparent and verifiable markets for perpetual contracts.

-

Reduces dependence on centralized matching layers or opaque matching policies.

-

Enables programmatic trading via smart contracts, unlocking automation and strategy composability.

-

Reinforces trust through state traceability, consensus validation, and reproducibility of every trade path.

4.4 On-Chain Matching Engine

The matching engine is the heart of TradeView’s execution pipeline, responsible for deterministically pairing buy and sell orders directly on-chain. Unlike off-chain models where matching logic is opaque or vulnerable to MEV, TradeView’s matching engine is embedded within its Layer-1 protocol. It ensures fairness, atomicity, and speed — all within the bounds of decentralized consensus.

4.4.1 Architectural Design

-

*Native Smart Contract Matching Logic*

-

Fully implemented in WASM-compatible smart contracts.

-

Every match is processed via deterministic logic validated by all consensus nodes.

-

No external scripts, bots, or sequencers influence the match outcome.

-

-

*Order Matching Triggers*

-

Matches are triggered during:

-

New order placement events.

-

Cancellations that unlock liquidity for price-level improvement.

-

Expiring conditional orders that activate upon market conditions.

-

-

Matching can also be batch-triggered at the block level for bulk execution events.

-

*Execution Context Isolation*

-

Matching logic is modularized from the order placement engine.

-

Operates on in-memory order snapshots built from the current block state.

-

Enables hot-swapping of matching logic per market type (e.g., perps vs. spot).

4.4.2 Matching Algorithms and Logic

TradeView’s on-chain matching engine is engineered for performance-grade fairness, supporting a broad range of trading scenarios while mitigating MEV risks and maintaining execution determinism. The logic is fully implemented in smart contracts and is optimized for latency-sensitive strategies and institutional-grade order flow.

Key Matching Mechanics:

-

*Price-Time Priority Enforcement*

-

Orders are matched first by best available price, and then by earliest timestamp.

-

At each price level, a FIFO queue is strictly maintained to ensure fairness and eliminate front-running.

-

This sequencing is enforced at the consensus level and exposed for public validation via API.

-

-

*Market Order Sweeps*

-

Market orders sweep the top of the book, consuming liquidity until the specified quantity is filled.

-

Supports partial fills, with unfilled quantities optionally queued as limit orders based on user-defined constraints.

-

This flow ensures slippage control without breaking atomicity or execution integrity.

-

-

*Advanced Matching Scenarios* The engine supports advanced conditional logic, including:

-

TWAP/VWAP Segmentation: Orders are sliced into timed buckets for algorithmic execution over a defined interval.

-

OCO (One-Cancels-the-Other): Execution of one leg triggers automatic cancellation of the paired order.

-

Iceberg Orders: Hidden order sizes are progressively revealed during execution, without disclosing total intent prematurely.

-

-

*Overflow & Rollover Logic*

-

Handles excess liquidity gracefully through smart buffer management, avoiding skipped ticks or forced reverts.

-

Rollover buckets are used during periods of extreme volatility to prevent overshooting or stale fills, ensuring price stability and fair execution under stress.

-

MEV-Aware Design:

-

The matching engine blocks arbitrary transaction reordering through consensus-layer validation.

-

Batch auction logic is optionally supported to enforce uniform pricing in high-volume blocks.

-

All matching decisions are fully transparent, and validators are subject to slashing if sequencing rules are violated.

4.4.3 Data Handling and Memory Efficiency

-

*In-Memory Snapshot Trees*

-

Matching is computed on ephemeral in-memory representations of the order book per block.

-

Reduces I/O load and speeds up reconciliation for validators.

-

-

*Sparse Execution Paths*

-

Only matching-active markets are evaluated each block to reduce computation cost.

-

Idle markets are skipped unless explicitly pinged by new placement transactions.

-

-

*Compressed Output Encoding*

-

Fill reports and trades are encoded into compact transaction logs.

-

Optimized for off-chain indexing and L2 mirroring.

-

4.4.4 Integrity and Validation

-

*Consensus-Level Enforcement*

-

Matching results are part of the state transition and block proposal.

-

Validators verify a deterministic outcome based on the canonical order book.

-

-

*Reproducibility Across Nodes*

-

Identical input state = identical output matches across all nodes.

-

Prevents front-running, inconsistent fills, or timestamp gaming.

-

-

*Slashing Hooks*

-

Validators proposing inconsistent match results face automatic slashing.

-

Provides cryptoeconomic security guarantees against tampering.

-

4.4.5 Smart Contract Interfaces

-

*Matcher Contract Module*

-

Stateless execution logic that consumes sorted price queues and emits trades.

-

Accepts hinting from placement transactions (optional, for gas efficiency).

-

-

*Trade Settlement Hooks*

-

Matches are streamed directly to the settlement module for margin adjustment and PnL resolution.

-

Supports dual-path execution: atomic with placement, or batched at block close.

-

4.4.6 Performance Optimizations

-

*Block-Level Batching*

-

Matching computation occurs post-order placement batch, reducing contention.

-

Supports large volume events like liquidations or airdrop-triggered surges.

-

-

*Gas Efficiency via Pre-Hinting*

-

Orders can optionally include a “match hint” (suggested price bucket) to accelerate lookup.

-

If the hint is correct, matching is a shortcut, and if incorrect, fall back to full search.

-

-

*Parallel Match Execution (Experimental)*

-

The future roadmap includes partial parallelization of matches across non-overlapping markets.

-

Could leverage multi-core validator execution environments.

-

4.4.7 Transparency and Composability

-

*Event-Emitted Match Reports*

-

Every matched trade emits standardized on-chain logs for:

-

Price

-

Size

-

Maker and taker addresses

-

Order IDs and timestamps

-

-

Enables full real-time reconstruction of the tape by any external observer.

-

-

*Composable Output Format*

-

Matching output is designed to integrate with:

-

PnL engine

-

Liquidation triggers

-

Cross-chain reporting modules

-

On-chain strategy vaults (TWAP trackers, hedging bots)

-

-

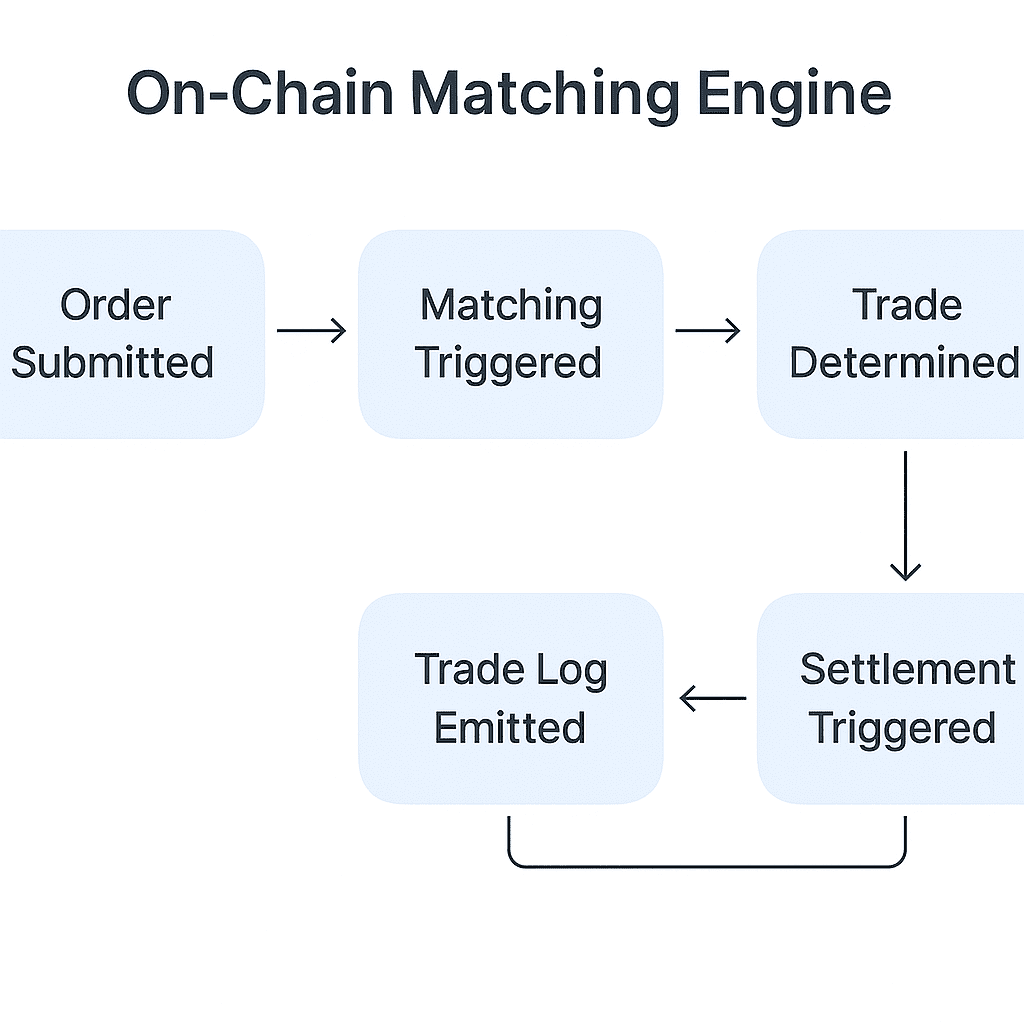

4.4.8 Order Match Lifecycle Trace

-

Order Submitted → Placement module appends to in-memory queue.

-

Matching Triggered → Best-price scan occurs (maker side first).

-

Trade Determined → Quantity match, price resolution, side identification.

-

Trade Log Emitted → Structured event for external oracles and analytics.

-

Settlement Triggered → Funds transferred, margin recalculated, fees deducted.

Why It Matters

-

Ensures MEV-resistant, tamper-proof trade execution

-

Removes the need for centralized or off-chain order routers

-

Maintains fairness during volatile markets or peak loads

-

Supports advanced order types and real-time trade logic at the protocol layer

-

Creates a verifiable and composable trade log for vaults, bots, and analytics tools

4.5 On-Chain Trade Execution Environment (Placement → Matching → Settlement)

The on-chain trade execution environment in TradeView is engineered for precision, speed, and transparency. Built on top of a custom Layer-1 and integrated tightly with the Tendermint BFT consensus, it ensures deterministic, gas-optimized execution of perpetual futures trades in a fully trustless setting.

4.5.1 Order Placement Layer

- Transaction Input Normalization

-

Trade intents are submitted via wallet, DApp, or automated API calls.

-

Payloads include: order type, quantity, limit price, margin mode, leverage, nonce, and user signature.

-

All input payloads undergo a normalization process before entering the mempool:

-

Verifies schema compliance.

-

Validates base asset and quote asset formats.

-

Normalizes decimals to the protocol-level standard.

-

-

Input is hashed using SHA-256 or Keccak-256 and compared against existing transaction hashes to prevent replay attacks and duplicate processing.

- Signature Verification & Pre-Execution Checks

-

Wallet signatures are validated using ECDSA (or Schnorr, if configured via chain runtime).

-

Balance checks are run against the user’s USDC wallet and any whitelisted collateral pool (e.g., stETH vault).

-

Margin sufficiency is calculated per:

-

Leverage selected.

-

Initial margin requirement.

-

Any active funding or haircut modifiers.

-

- Nonce Management and Queuing

-

A global and per-user nonce model ensures deterministic order sequencing.

-

Orders are added to the block’s in-memory execution queue, tagged with:

-

Block height.

-

Submission timestamp.

-

Gas cost estimate (for non-trading ops).

-

-

The queue feeds into the matching engine during block execution.

4.5.2 Matching Engine Interface (Execution Trigger)

- Atomic Integration

-

Order handoff is performed via intra-chain module calls using Cosmos-SDK's inter-module message passing.

-

The call is atomic:

-

Either it completes in full or reverts.

-

Prevents partial fills, broken states, or cross-validator inconsistency.

-

- Matching Protocol

-

Orders are matched using a deterministic price-time algorithm:

-

First, by the best price.

-

Then, by the earliest nonce for tie-breaking.

-

-

Match constraints include:

-

Margin availability.

-

Volatility bounds (prevent slippage).

-

Oracle freshness (within the last N seconds).

-

-

Execution generates a "Match Intent," which includes:

-

Trade price and volume.

-

Taker/maker roles.

-

Execution latency (for slippage monitoring).

-

Fee tiers applied.

-

4.5.3 On-Chain Trade Settlement

- Real-Time Asset Flow

-

Trades trigger real-time collateral updates:

-

Margins are debited and credited at sub-second speed.

-

Positions are updated in the state tree — size, entry price, realized PnL, and funding delta.

-

-

Oracle feeds re-sync after settlement to provide updated unrealized PnL snapshots.

- Event Broadcasting

-

Every settlement emits multiple event logs, including:

- TradeExecuted, PositionOpened, PositionModified, PositionClosed, LiquidationTriggered.

-

Events are signed, timestamped, and batched per block for fast indexing.

-

TradeView provides a real-time pub-sub relay for bots and UIs to subscribe.

- Finality Guarantees

-

Thanks to Tendermint's instant finality:

-

Once a trade is confirmed in a block, it is irreversible.

-

Rollbacks or reorganizations are cryptoeconomically infeasible.

-

4.5.4 Fee Handling and Gas Efficiency

- Gas Abstraction Model

-

Trading operations are subsidized by protocol-level incentives:

-

Most trades incur nearly 0 gas fees.

-

Heavy operations (e.g., cancellations, batch edits) incur nominal gas, paid in native token.

-

-

Validators are compensated via block rewards and emissions, not trading gas fees.

- Dynamic Fee Distribution

-

Fees collected from trading are split via smart contract logic:

-

X% to Treasury (for growth, buybacks).

-

Y% to Referrer (if trade includes a referral tag).

-

Z% to the Insurance Fund.

-

-

Fee routing is configurable via on-chain governance proposals.

-

Supports retroactive rewards and gamified incentives (e.g., top-volume leaderboard rewards).

4.5.5 Error Handling & Fallback Logic

- Rejection Scenarios

-

Orders are rejected before matching if:

-

Margin is insufficient (post-price update).

-

Oracle data is stale beyond the tolerance threshold.

-

Submitted trade violates market bounds (e.g., price cap/floor).

-

-

Rejections emit OrderRejected logs with error codes:

-

101: Margin Error.

-

102: Oracle Delay.

-

103: Execution Unsafe.

-

- Revert Logic

-

All critical contract calls are wrapped in try/catch blocks using Go’s panic recovery in Cosmos SDK.

-

Validators store reverts in local logs and hash these into the block result for transparency.

-

Replay-safe — a reverted order will never be processed again due to nonce locking.

4.5.6 Settlement State Synchronization

- Block-Level State Commit

-

Each Tendermint block commits:

-

Full order book delta.

-

Updated positions ledger.

-

Vault balance changes (if collateral flows involved).

-

-

State root (Merkle) is committed and pinned as proof for cross-chain syncing.

4.5.6.2 Indexing and Archival Hooks

-

On every match and state change:

-

A pre-configured TxHook module logs the delta.

-

State deltas are streamed to indexers (e.g., The Graph, SubQuery).

-

-

This supports:

-

Portfolio dashboards.

-

Tax compliance reports.

-

External DeFi analytics platforms.

-

CEX-Like Speed Without Central Control What’s the point of building an on-chain matching engine and execution environment from scratch? For investors, it boils down to this: - Latency and finality are on par with centralized exchanges — but without a centralized operator or custodian. - Orders execute deterministically — no partial fills lost in mempools, no MEV bots jumping the queue. - Matching logic is public and auditable, meaning execution is fair, reproducible, and governed by code — not by opaque CEX matching logic. - Unlike most DEXs that simulate trades off-chain and finalize them later, TradeView does everything natively on its L1 — so vaults, bots, and traders don’t need workarounds or trust assumptions. For traders and partners alike, this is the holy grail: the execution speed and reliability of a Binance or Coinbase — but underpinned by transparent code, DAO governance, and non-custodial access.

4.6 Account System

TradeView’s account system is the backbone for identity, balance tracking, position management, access control, and integration across components of the platform. It is designed to handle the complexity of modern DeFi users—from single-address retail traders to institutions with role-based permissions—while remaining entirely on-chain.

4.6.1 Unified Account Abstraction Layer

-

*Abstracted User Identity:* Accounts are not tied directly to EOAs (externally owned accounts); instead, they are abstracted smart contract-based entities, enabling key flexibility, modularity, and composability.

-

*Address-Agnostic Interaction:* The system supports multiple identity types (wallets, email-based custodial access, API keys) mapped to a single account structure.

-

*Nonce Management:* Custom nonce tracking enables parallel transactions, off-chain message batching, and gasless trade authorizations.

-

*Programmable Control Logic:* Every account supports embedded access rules, withdrawal delays, trade execution logic, and integration with automation frameworks like keepers or bots.

4.6.2 Multi-Asset Balance Management

-

*Real-Time Ledger System:* Each account maintains sub-ledgers for every collateral asset supported (USDC, stETH, ETH, LP tokens, etc.) with on-chain reconciliation on every state transition.

-

*Modular Balance Modules:* Asset balances are managed via plug-in modules that apply specific rules—e.g., for rebasing tokens, staked yield accounts, or tokenized strategies.

-

*Cross-Chain Collateral Routing:* Account balances support synthetic asset mirrors, allowing users to deposit on one chain and use it as collateral elsewhere without bridging delays.

-

*Partial Freezing Mechanism:* For liquidation and risk control, specific portions of an account’s balance can be locked while leaving the rest operable.

4.6.3 Position Tracking & Margin Management

-

*Isolated and Cross-Margin Modes:* Each account can toggle between isolated margin (per-position collateralization) or cross-margining (pooled collateral usage), with different risk tolerances.

-

*On-Chain Unrealized PnL Calculation:* Positions are marked-to-market in real time using oracle feeds and internal pricing engines.

-

*Liquidation Flags & Buffers:* Every account includes configurable risk thresholds, liquidation delays, and safety margins for controlled exposure.

-

*Funding & Fee Accrual Subsystem:* Funding payments, maker-taker fees, and rebate distributions are tracked at the account level with per-epoch granularity.

4.6.4 Role-Based Permissions & Delegation

-

*Multi-Key Account Architecture:* An account can have multiple authorized signers with different access scopes—ideal for institutions, bots, or DAOs.

-

*Permission Classes:* Defined access tiers include:

-

Trader

-

Depositor

-

Vault Manager

-

Risk Admin

-

Governance Delegate

-

-

*Programmable Delegation:* Permissions can be time-bound, logic-bound (e.g., only trade BTC perpetuals), or even externally governed via DAO signatures or wallet whitelists.

-

*Secure Key Rotation:* Role keys can be replaced via on-chain governance or time-delayed security modules to prevent hijack attempts.

4.6.5 Custodial and Non-Custodial Account Support

-

*Web2-Friendly Integration:* Custodial email/password users are abstracted into full smart contract accounts on-chain, with key management offloaded to MPC custodians or device-bound secrets.

-

*Upgradeable to Full Self-Custody:* Custodial accounts can be migrated to user-controlled keys, keeping all balances, PnL history, and access rights intact.

-

*Session Key Authorization:* Short-lived keys can be issued to frontends or bots for non-sensitive actions like querying balances or creating draft orders, without exposing full control.

4.6.6 Trade Execution Integration

-

*Atomic Order Placement:* Orders are placed as signed transactions that directly invoke position updates within the account module.

-

*Batch Execution Paths:* Multiple trades, cancellations, and margin updates can be batched for gas savings and time-sensitive strategies.

-

*Vault-Aware Orders:* Accounts are aware of vault participation, enabling order execution based on vault constraints or triggers.

-

*Fallback Mechanisms:* In case of matching engine downtime or delayed settlement, account modules store pending deltas for later reconciliation.

4.6.7 Data Availability & Query Architecture

-

*Merkleized Account State:* Account data is part of the chain’s Merkle root, enabling zero-knowledge proofs and off-chain synchronization.

-

*Subgraph-Compatible APIs:* Real-time data is streamed via indexing services that map account balances, trade history, liquidations, and vault participation for frontend consumption.

-

*Encrypted Metadata Channels:* Optional off-chain metadata like device type, biometric session, or email mappings can be encrypted and tied to account roots without exposing PII on-chain.

4.6.8 Auditability and Risk Monitoring

-

*Chain-Wide Account Health Reports:* The protocol periodically computes account-level and system-wide metrics—total margin utilization, net open interest, cross-asset risk—for governance or emergency actions.

-

*Historical Traceability:* Every action (deposit, order, withdrawal, rebalance) is logged immutably, enabling full audit trails for institutional oversight.

-

*Compliance Hooks:* While zero-KYC is preserved, pluggable modules can allow optional identity attestation or geographical filtering for use cases like institutional vaults or regulated deployments.

4.7 Cross-Chain Bridges

The Cross-Chain Bridge subsystem in TradeView is a foundational pillar that enables decentralized collateral movement and capital interoperability across multiple blockchain ecosystems. Unlike traditional centralized bridges or wrapped asset protocols, TradeView’s bridge system is designed with trust-minimized architecture, real-time settlement capabilities, and modular extensibility to support L1s, L2s, and app-chains with diverse virtual machines and consensus mechanisms.

4.7.1 Architecture Overview

-

Bridge Contracts on Source Chains

-

Smart contracts deployed on external chains (Ethereum, Solana, Base, Polygon, etc.)

-

Facilitate locking of user assets (e.g., USDC, ETH, stETH, rsETH)

-

Emit events upon deposit to signal the intention of cross-chain collateral usage

-

-

IBC-style Proof Relay Mechanism

-

Off-chain relayers or light clients monitor source chain events

-

Submit Merkle proofs or header-derived attestations to TradeView’s native chain

-

Ensures the cryptographic authenticity of deposit/withdrawal actions

-

-

TradeView Ingress Module

-

Accepts verified cross-chain proofs

-

Mints synthetic representations (e.g., xUSDC, xstETH) as collateral

-

Ties them to the originating address’s TradeView account via canonical vaults

-

4.7.2 Canonical Vaults and Synthetic Minting

-

Canonical Vault Contracts

-

Maintain balance sheets of all synthetic collateral minted via bridging

-

Track asset type, deposit origin, and associated liquidation thresholds

-

-

Synthetic Token Standardization

-

Each bridged asset is represented by a synthetic (1:1 soft-pegged) token

-

Includes metadata such as originating chain, token type, and oracle source

-

Allows composability with the TradeView margin engine and risk layers

-

-

Non-Custodial by Design

-

TradeView chain never controls native assets; it only issues collateral claims

-

Redeemability is governed by reverse proofs, not centralized approval

-

4.7.3 Withdrawal and Exit Flow

-

TradeView Egress Module

-

Users initiate withdrawal from the TradeView chain

-

The synthetic token is burned, triggering a withdrawal intent proof

-

-

Exit Proof Submission

-

Relayer or user submits signed withdrawal proof to the source chain bridge contract

-

Verifies burn, timestamp, and associated signature payload

-

-

Native Asset Release

-

Upon verification, the locked asset is released back to the user

-

Can be programmatically routed to wallet, yield strategy, or off-ramp module

-

4.7.4 Fast Finality Layer and Optimistic Confirmation

-

Instant Credit Layer (Optional)

-

Validators or bonded relayers may offer instant asset credits based on mempool-level bridging signals

-

Risk mitigated by stake slashing in case of malicious or false relaying

-

-

Timeout and Recovery Logic

-

If message delivery fails due to relayer downtime, users can initiate manual redemption via fallback proof

-

Timeout constraints prevent duplicate or spoofed settlements

-

4.7.5 Security Assumptions and Slashing

-

Validator Participation in Relaying

-

Validators or appointed bridge agents are responsible for proof forwarding

-

Misbehavior (e.g., double-minting or withholding proofs) results in slashing from the staking module

-

-

Multi-Sig or Light Client Verification

-

Depending on the chain, TradeView supports:

-

Multi-sig verification (for fast bridges)

-

On-chain light client verification (for IBC-style models)

-

-

-

Auditability & Transparency

-

All bridge messages and proof transactions are stored on-chain

-

Fully auditable by the community, users, and third-party security agents

-

4.7.6 Supported Chains and Extensibility

-

Initial Chain Support

-

Ethereum (Mainnet)

-

Solana

-

Arbitrum, Optimism, Base

-

Polygon POS

-

-

Pluggable Bridge Adapters

-

Modular architecture enables support for new chains via adapter contracts

-

No need to recompile TradeView core contracts

-

New adapters undergo governance or validator approval

-

4.7.7 Bridge Abstraction in the Developer Stack

-

Bridge API Layer

-

Exposes REST/gRPC endpoints to UI clients, vault managers, and bots

-

Handles:

-

Status of bridging operations

-

Estimated confirmation time

-

Wallet-based bridging instructions

-

-

-

Bridge SDK

-

JavaScript and Rust SDKs to enable dApps or strategy builders to integrate bridge features

-

Includes wallet hooks, transaction encoders, and off-chain proof verifiers

-

4.7.8 Key Technical Advantages

-

No Custodial Risk

- No assets are held by TradeView — all value is locked in source chain bridge contracts

-

Native Chain Yield Preservation

- Users retain yield rights on LSTs or LRTs even while using their synthetic form on TradeView

-

Real-Time Proof Handling

- Messages are processed block-by-block with tight consensus synchronization, enabling near-instant synthetic minting

-

Resilient to Network Downtime

- TradeView supports fallback queues and off-chain proof recovery, ensuring bridge liveness even during congestion

4.7.9 Outcome: Unified Liquidity Across Chains

-

TradeView’s bridge system is not just a transfer layer — it is a collateral coordination protocol.

-

Assets from Ethereum, Solana, or L2s can be brought into TradeView’s execution environment without fragmentation

-

Margin can be posted, managed, and withdrawn without leaving the chain of origin

-

This delivers a truly cross-chain DeFi trading experience without compromising speed, security, or composability

-

4.8 Vaults, Bots, APIs

TradeView's ecosystem is structured to support robust programmatic interfaces and modular automation layers. This allows third-party strategies, bots, and user-defined vaults to operate natively within the protocol without compromising security or performance. The components described below are critical in enabling non-custodial composability, reactive automation, and granular integrations.

4.8.1 Vault Architecture

-

*Modular Vault Contracts* Each vault is instantiated from a verified smart contract template that conforms to a vault interface standard. These templates are upgradeable via governance-controlled registries to ensure extensibility while preserving auditability.

-

*Multi-Asset Support* Vaults can accept diverse collateral types, including stablecoins, LSTs, LRTs, and TradeView-native tokens. The architecture ensures dynamic handling of LTVs, slippage, and on-chain pricing sources per asset.

-

*Strategy Execution Layer* Vault logic can embed or reference programmable strategies — such as market-making scripts, yield optimizers, TWAP/VWAP schedulers — using conditional triggers defined at the contract level.

-

*Permissionless Deployment* Vault deployment is open to verified users and developers, but contracts must pass static analysis checks and gas profiling to be whitelisted on-chain.

-

*Isolated Risk Domains* Vaults maintain isolated accounting and liquidation logic, ensuring faults in one strategy do not impact system-wide solvency.

-

*Integrated Liquidation Handlers* Vaults can register fallback liquidation logic to define exit paths if collateralization falls below a threshold (e.g., swap to stables, exit perps, auto-deleveraging).

4.8.2 Bot Framework & Automation Hooks

-

*On-Chain Event Subscriptions* TradeView supports event hooks (e.g., funding rate updates, volatility breaches, margin proximity) that bots can subscribe to via public endpoints or WebSocket feeds.

-

*Bot-to-Chain Gateways* Bots operate via authenticated relayers that sign messages against non-custodial keys. This allows automated execution without direct private key exposure.

-

*Off-Chain Computation Modules* For intensive tasks like backtesting, machine learning-based rebalancing, or gas optimization, bots can use off-chain workers that post proofs or signed payloads back to the chain.

-

*Rate-Limiting and Anti-Spam Filters* To ensure stability, each bot address must register through a verification mechanism and obey on-chain rate caps and failover rules enforced at the protocol gateway layer.

-

*Gas Abstraction for Bots* Bots operating on behalf of users can use meta-transaction relayers, allowing end-users to interact gaslessly while retaining deterministic execution.

4.8.3 Public APIs & Developer Tooling

-

*TradeView REST & WebSocket APIs* Fully documented endpoints support:

-

Order management (create, cancel, modify)

-

Position queries and account history

-

Funding and oracle rates

-

Vault performance and risk metrics

-

Governance voting state

-

-

*API Authentication* OAuth 2.0-style token flow layered over signature verification ensures that third-party dashboards and apps can authenticate safely on behalf of users.

-

*Rate-Limited Throttling for Fair Usage* API endpoints are rate-limited per key and IP class to ensure platform reliability, with burstable quotas for high-throughput applications like analytics dashboards and trading terminals.

-

*SDK Support* Developer SDKs (planned in TypeScript, Python, and Go) allow direct integration with key ecosystem primitives such as:

-

Vault deployment modules

-

Trading and portfolio dashboards

-

On-chain risk analysis tools

-

Custom strategy runners

-

-

*GraphQL Support (Planned)* Future iterations include a dedicated GraphQL interface for querying indexed data across accounts, vaults, governance decisions, and historical trade actions.

4.8.4 Execution Sandboxing and Governance

-

*Governance-Approved Modules* Each bot, vault, or third-party contract must pass a governance approval path to be visible on public dashboards or to integrate with incentives.

-

*Deterministic Execution Sandbox* Strategies and automation contracts execute within the deterministic bounds of the TradeView L1, using block-level atomicity and signature-based controls to ensure state validity.

-

*Audit Layer and Monitoring* All third-party vaults and automation hooks are monitored by an on-chain registry that logs:

-

Performance metrics

-

Slippage vs. benchmarks

-

Failure rate

-

Gas usage per invocation

-

-

These logs are auditable both by governance and external tooling.

4.8.5 Interoperability and Upgrade Path

-

*Cross-Contract Composability* Vaults and bots can interact with other modules via standard interfaces, enabling nested strategies (e.g., vaults that tap into other vaults, bots triggering orders across pools).

-

*Upgradeable Proxy Standard* Contracts follow a controlled proxy pattern where upgrades are limited to logic changes — state migrations must follow strict snapshot protocols.

-

*Versioning and Compatibility Flags* Each vault or bot registers with a versioning identifier to ensure backward compatibility and prevent logic drift in long-running automated contracts.

TradeView’s modular design for vaults, bots, and APIs unlocks a robust automation and strategy layer without compromising the core protocol’s determinism, security, or composability. This ecosystem enables the next generation of DeFi-native trading infrastructure — programmable, permissionless, and performance-aligned.

4.9 Performance Benchmarks and Stress Testing

A decentralized trading platform is only as good as its ability to perform under real-world conditions. TradeView's architecture is built not only for theoretical throughput, but for sustained, real-time performance across high-volume, high-concurrency, and high-latency environments. This section outlines the benchmarking methodology, technical metrics, and stress-testing frameworks that define the operational limits and resilience of TradeView’s infrastructure.

4.9.1 Benchmarking Environment Configuration

-

Testnet Cluster Composition

-

Simulated network with 32 full validators running Tendermint BFT

-

4 archival nodes for load replication

-

Global latency injection (50–300ms) for realistic geo-distributed testing

-

-

Hardware Specification

-

Validator nodes run on 8-core CPUs, 32 GB RAM, and SSD-backed storage

-

Load testers simulate clients via AWS Fargate & bare metal for realism

-

On-chain database backed by optimized IAVL Merkle tree structures

-

-

Load Generation Tools

-

An internal benchmarking suite written in Go simulates:

-

Order flow with random/structured patterns

-

Vault updates, rebalancing events

-

Governance, staking, and account actions

-

-

Rate ramping modules increase requests from 500 to 50,000 TPS to observe breaking points

-

4.9.2 Core Metrics Captured

-

Transactions Per Second (TPS)

-

Baseline: ~11,500 TPS for standard order traffic

-

Peak: Surges up to 13,700 TPS under full CPU utilization

-

Latency remains sub-1s until the 95% threshold

-

-

Block Finality Time

-

Median finality: 680ms

-

99th percentile: <900ms under load

-

No observable rollback or validator stalls below 33% faulty threshold

-

-

Matching Engine Throughput

-

Can resolve 1,000+ matches per block

-

Limit/cancel/modify orders handled within the same execution frame

-

Deterministic conflict resolution benchmarked with simulated orderbook congestion

-

-

Collateral Sync Latency (Cross-Chain)

-

Oracle update propagation under 3s

-

Synthetic asset mint and burn latency within 5s roundtrip

-

IBC-style proofs verified using Merkle trees at <1.2s average latency

-

-

Vault Execution Timing

-

Single strategy: ~250ms from trigger to rebalance

-

Concurrent vault operations: scaled to 200 concurrent vaults without degradation

-

Average gas per rebalance: 230k

-

-

Staking & Governance Event Lag

-

Delegation/undelegation: <2 blocks

-

Proposal registration → vote open: <5s

-

Vote tally and implementation after quorum: <30s

-

4.9.3 Stress Testing Protocols

-

Load Amplification Scenarios

-

Spike orders: Simulate arbitrage bots submitting 5k–15k transactions in <3 seconds

-

Front-running attempts: Synthetic latency exploit simulations to test consensus order integrity

-

Vault flash cycles: Rapid margin changes with volatile collateral sources

-

-

Failure Injection

-

Validator downtime up to 25% nodes

-

Double-sign attempt to test Tendermint slashing response

-

Storage bloat tests to evaluate Merkle proof latency with millions of historical state entries

-

-

Persistence Degradation Tests

-

Evaluate order and state retention under disk read/write pressure

-

Simulated node restarts and memory leaks

-

Benchmarked recovery time from node snapshot: <3 minutes to resync full ledger

-

-

Bridge & Cross-Chain Latency Under Duress

-

Flood Ethereum L1 with 10k deposits to test bridge queueing

-

Simulated relayer failures and packet reordering

-

Asset reconciliation & retry logic confirmed via replay-safe proofs

-

4.9.4 Tooling & Observability Stack

-

Real-Time Monitoring Interfaces

-

Prometheus + Grafana dashboards tracking:

-

CPU, memory, I/O utilization

-

Block height, transaction inclusion delay

-

Error rates and validator signature misses

-

-

-

Historical Traceability

-

All major events (trade, liquidation, governance vote) are indexed with:

-

Block height

-

Execution gas profile

-

State diff snapshot

-

-

-

Error Handling & Alerts

-

On-chain and off-chain alerts via PagerDuty integrations

-

Transaction failure codes linked to developer-facing diagnostics

-

Post-mortem logs tagged and auto-exported for root cause analysis

-

-

Dev/Test Automation Coverage

-

92% smart contract coverage with fuzz testing

-

Unit and integration tests are executed on every new vault or strategy deployment

-

Simulated testnet resets weekly to observe full chain resilience

-

4.9.5 Key Takeaways from Benchmarking

-

TradeView’s custom Layer-1 stack consistently handles 10,000+ TPS with sub-second finality, even under stress.

-

Vaults, bots, and cross-chain components maintain performance without compromising deterministic execution or validator consensus.

-

Systemic failure points are mitigated through redundancy, observable hooks, and deterministic state integrity, positioning TradeView as an enterprise-grade DeFi backend.

4.10 MEV Mitigation Architecture

In a high-speed, high-stakes environment like perpetual trading, every microsecond of execution timing, order positioning, and liquidation flow can be monetized, or exploited. While on-chain transparency is one of DeFi’s core strengths, it also exposes protocols to a class of sophisticated attacks known as Miner/Maximal Extractable Value (MEV).

Unlike price manipulation or oracle failure, MEV is insidious, it doesn’t break the rules of the system, it bends them for private gain. Bots front-run user orders. Validators reorder blocks to benefit their vaults. Liquidations are sniped mid-execution. And the worst part? It’s often invisible to the very traders losing money because of it.

For on-chain perpetual platforms, MEV is not a “security issue.” It’s an economic integrity issue, one that impacts fill fairness, liquidation trust, capital retention, and ultimately, protocol reputation.

TradeView’s MEV mitigation is not bolted on, it’s embedded at the protocol layer. From how orders are queued and matched, to how liquidations are processed and block producers behave, MEV resistance is treated as a design constraint across the full execution stack.

Investor Note: What is MEV — and Why It’s Bad for Traders? MEV stands for Maximal Extractable Value — it’s the practice of extracting extra profit by reordering, inserting, or censoring transactions on a blockchain before they’re finalized. Here’s how it hurts you: - Front-running: A validator sees your profitable trade in the mempool and slips in their own trade just ahead of yours — eating your profits. - Sandwich attacks: You buy a token, they buy before you and sell after you — and your slippage becomes their gain. - Order manipulation: In a volatile market, milliseconds matter. MEV lets insiders reshuffle the order queue, breaking the price you thought you’d get. These tactics are common on chains where validators control execution and where trading happens on public mempools — like Ethereum or most L2s. Why TradeView Fixes This - TradeView’s custom L1 and Tendermint-based consensus means no probabilistic forks and no validator games. - The matching engine is on-chain and deterministic — no room to sneak in sandwich trades or rearrange orders. - Mempools are prioritized by intent type, not tip bribes — ensuring liquidations, funding updates, and vault logic stay fair. Bottom line: With TradeView, traders — not validators — get to decide how orders are executed.

4.10.1 Why MEV Mitigation Matters in On-Chain Perpetual Trading

The promise of a fully on-chain trading system is built on fairness, transparency, and user protection. But these ideals are often compromised by a subtle, invisible threat: Miner/Maximal Extractable Value (MEV), which refers to the ability for validators or bots to manipulate transaction ordering for financial gain.

While MEV may be tolerable in basic token swaps or NFT mints, in perpetual trading, it’s a deal-breaker, especially for high-frequency, leveraged, or institutional strategies. At best, MEV introduces slippage. At worst, it creates an unfair playing field where informed participants consistently extract value at the expense of others.

Here’s why TradeView treats MEV mitigation not as a feature, but as a foundational requirement.

- What Is MEV in the Context of Perpetual Trading?

-

Sandwich Attacks:

An attacker spots a large pending trade in the mempool, places a buy before it and a sell after it — profiting from predictable price movement.

→ The victim gets a worse fill than expected. -

Front-Running:

A validator or bot sees a liquidation or breakout trade queued and rushes a competing trade ahead by paying higher gas or manipulating ordering.

→ Profits by stealing the priority or triggering downstream market movement. -

Back-Runs on Liquidations:

After a liquidation is triggered, MEV bots try to back-run for cheap asset acquisition, especially if slippage penalties are expected.

→ This undermines the insurance fund’s stability and fairness of execution. -

Validator Reordering:

Validators can rearrange transaction order within a block to benefit their own trades, vaults, or bots — an exploit not obvious to average users.

→ This creates non-transparent latency arbitrage, replicating the same problem DeFi was built to solve.

- Why This Is a Major Problem for Real Traders

-

*Destroys Predictability for Market Makers* Market makers, HFTs, and institutions rely on tight spreads and timing guarantees. MEV breaks this by injecting randomness and slippage into execution.

-

*Undermines Strategy Bots and TWAP Orders* Advanced strategies like TWAP/VWAP or iceberg orders become exploitable targets — their intent is visible, but their execution isn’t protected.

-

*Weakens Confidence in On-Chain Settlement* If traders believe their transactions can be front-run or reordered, they’ll migrate back to centralized exchanges or hybrid rollup models.

-

*Incentivizes Toxic Order Flow* Sophisticated bots start optimizing for extraction, not liquidity — leading to more volatility, higher gas fees, and degraded user experience for others.

- Why Perpetuals Are Especially Vulnerable

-

Unlike AMMs, perpetuals involve leverage, margin, and liquidations — timing is everything.

-

MEV here doesn’t just skim value — it creates systemic risk:

-

Bad liquidations → unnecessary user loss

-

Order book imbalance → market instability

-

Insurance fund drain → protocol insolvency risks

-

- TradeView’s Stance on MEV

“A perpetual DEX is only as strong as its execution integrity. If you can’t trust the order of your trade, you can’t trust the protocol.”

That’s why TradeView enforces MEV-aware matching logic, validator rules, and sequencing safeguards as native design principles, not afterthoughts.

Every component, from order placement to liquidation, is audited for MEV surface area and reinforced to favor fair access over extractive edge.

4.10.2 Vulnerabilities in Typical On-Chain Matching

Despite the rise of decentralized trading, many DEX architectures still rely on flawed execution pipelines that open the door for MEV extraction. While the frontend may feel decentralized, what happens between “place order” and “order filled” is often opaque, manipulable, or outright centralized.

Let’s break down the most common vulnerabilities found in so-called “on-chain” perpetual DEXs — and why they fail to protect users from predatory ordering behavior.

- Off-Chain Matching Engines (The “DEX in Name Only” Problem)

-

Many platforms claim to be decentralized but still use off-chain order matching systems, often controlled by a single entity or backend API.

-

These systems receive all user orders but decide how, when, and whether to match them, giving insiders unfair control over:

-

Order sequencing

-

Price-time priority

-

Match-making between wallets

-

-

Traders cannot audit what actually happened — only the final matched result is sent on-chain.

-

This breaks the entire DeFi ethos: if execution isn’t on-chain, the protocol isn’t trustless.

- Sequencer-Based Rollups with Centralized Ordering

-

Many rollup-based perpetual DEXs rely on central sequencers to bundle and submit transactions to L2.

-

These sequencers act as gatekeepers, with power to:

-

Reorder trades for profit

-

Delay or censor transactions

-

Favor insider bots or pre-funded addresses

-

-

Even if execution logic is later verified on-chain, the ordering of events — the most critical part in trading — was not verifiable.

-

Result: deterministic smart contracts, nondeterministic execution.

- Insecure Mempools and Predictable Matching

-

On some L1-based DEXs, orders are sent unencrypted to public mempools.

-

MEV bots constantly scan these pools to:

-

Detect large market orders or liquidations

-

Insert their trades ahead of users (front-running)

-

Exploit visible intent in TWAP or iceberg strategies

-

-

This results in slippage for the user, profit for the attacker, and toxic order flow for the entire platform.

- Lack of Batch Auctions or Clearing Price Models

-

Most matching engines execute orders as soon as they arrive, creating a race where gas price = execution priority.

-

This creates:

-

Competitive bidding wars between bots

-

Unfair price discovery (e.g., first-to-fill wins even if both orders were valid at same time)

-

No protection for non-bot retail traders

-

-

Without batch auctions or clearing logic, platforms default to “fastest wins” — which isn’t decentralized, it’s just pay-to-play.

- No Anti-Self-Trade Mechanism

-

Without proper safeguards, users or bots can self-match their own orders.

-

This creates fake volume (wash trading) and manipulates:

-

Leaderboards

-

Trading incentives

-

Vault PnL and trust scores

-

-

Many DEXs still lack native detection for self-trading on-chain due to address abstraction, making the behavior hard to catch.

- The Institutional Gap

-

Institutions won’t bring capital to environments where execution can be gamed.

-

Lack of deterministic matching, transparent sequencing, or validator integrity makes on-chain perps unsuitable for:

-

Block trades

-

HFT integrations

-

Strategy vaults with real capital behind them

-

G. The Cost of Ignoring These Gaps

-

Real traders pay with slippage and loss of alpha.

-

Retail traders get priced out of their own trades.

-

Liquidity providers reduce exposure.

-

Protocols risk TVL outflows, legal scrutiny, and loss of long-term reputation.

*TradeView doesn’t patch over these flaws but it redesigns the matching layer to eliminate them.* In the next section, we’ll walk through how TradeView’s matching architecture makes MEV extraction practically unprofitable, and fair execution the default.

4.10.3 TradeView’s MEV Protection Framework

While many protocols attempt to patch MEV risks after the fact, TradeView incorporates MEV resistance at the architectural level, starting with how trades are submitted, sequenced, matched, and settled. The goal isn’t to simply reduce MEV but to make it economically irrational and technically infeasible to exploit.

TradeView’s framework consists of multiple layered defenses, designed to operate autonomously on-chain, without relying on trust in validators, off-chain relayers, or closed execution systems.

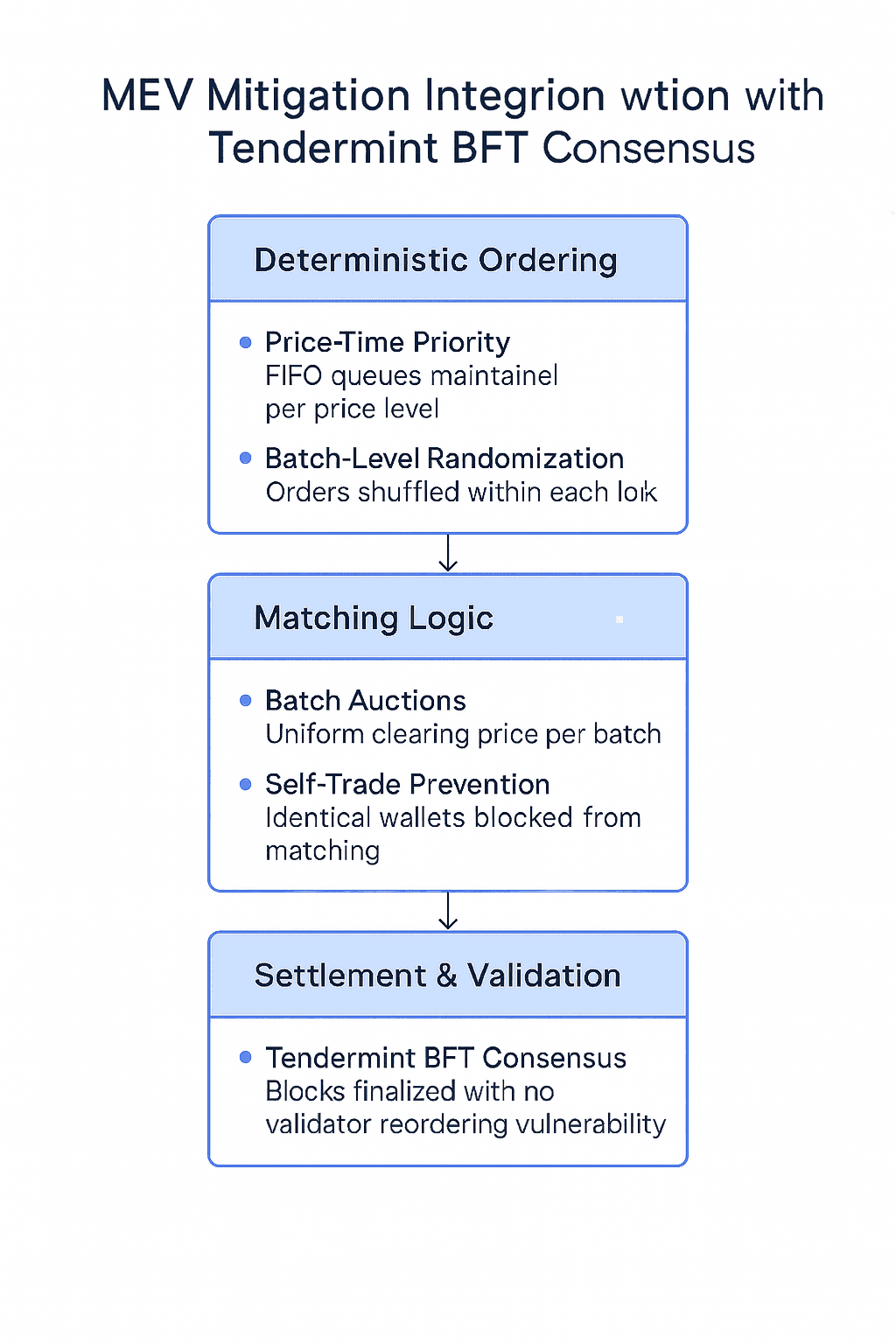

- Deterministic Transaction Ordering

-

Price-time priority is strictly enforced through on-chain logic. Orders at the same price level are executed in the exact order they were received — not the order of gas bids.

-

FIFO queues per price level ensure that no participant can “cut the line,” regardless of capital or compute advantage.

-

Validators cannot bypass this logic as block inclusion does not equate to execution privilege.

- Block-Level Batch Auctions

-

TradeView supports a batch auction mode, where all valid orders within a block are aggregated and cleared at a single uniform price.

-

This removes the incentive to snipe or rush transactions into a block, making timing advantage irrelevant.

-

Especially useful during volatile events or major listings, this ensures fair execution across participants, regardless of who submitted first by milliseconds.

- Randomized Sequencing for Equal Opportunity

-

Where strict FIFO enforcement is not optimal (e.g., during block congestion), TradeView introduces verifiable randomized sequencing of valid orders within the same priority bucket.

-

This prevents collusion between bots and validators and creates a level playing field where execution outcomes cannot be reliably gamed in advance.

- Self-Trade Detection and Prevention

-

TradeView natively blocks self-matching of orders submitted by the same wallet or controlled entity.

-

This ensures:

-

No fake volume

-

No manipulated leaderboards

-

No artificial vault performance

-

-

Address abstraction and bot relayers are accounted for preventing wash trading across multi-account setups.

- Liquidation Queue Fairness

-

Liquidations follow a time-based, eligibility-first queue. Even during volatility spikes, bots cannot leapfrog each other using gas auctions or private order flow.

-

No backdoor access, no validator favoritism, only the first valid triggerer gets the liquidation reward.

-

The protocol optionally supports batch liquidation rounds, which distribute liquidation execution rights fairly when multiple positions are eligible simultaneously.

—---------------------------------------------------------------------------------------------------------

TEXT FOR VISUAL

1. Order Submission Layer

-

Users sign and broadcast orders to the public mempool

-

TradeView's system tags orders with timestamp, price level, and wallet metadata

MEV Protection Applied:

-

Signature-verified timestamping (prevents manipulation of arrival time)

-

Address grouping logic (detects potential wash trade risk)

2. Sequencing & Queueing Layer

-

Orders enter deterministic FIFO queues per price level

-

If congestion occurs, optional randomized sequencing applies within equal-priority buckets

MEV Protection Applied:

-

No gas-based priority

-

Validators cannot influence intra-block sequencing

3. Matching Engine Execution

-

Orders processed via:

-

Price-time priority

-

Batch auction (optional per block)

-

-

Advanced orders (TWAP, OCO, Iceberg) executed using isolated logic

MEV Protection Applied:

-

No visibility advantage — all orders matched at clearing price

-

Conditional logic resolved on-chain, not by bots or relayers

4. Settlement & Liquidation Triggers

-

Settled trades update user balances and margin ratios

-

If margin breach detected, liquidation queue is activated

MEV Protection Applied:

-

Liquidation queues use time-based triggers, not gas

-

Batch liquidations prevent sniping

-

Self-liquidation exploits blocked by nonce + sig checks

5. Validator Enforcement Layer (Tendermint BFT)

-

Consensus validators propose and commit blocks

-

MEV attacks (reordering, censoring, delay) are not possible due to:

-

No mempool control

-

Deterministic execution logic

-

Validator slashing for deviation

-

—-------------------------------------------------------------------------------------------------------

No Whitelisted Actors. No Hidden Sequencers. No Gas Wars.

TradeView's on-chain execution stack is designed so fairness is guaranteed by architecture — not by good intentions.

- No Privileged Actors Ever

-

TradeView does not use hidden relayers, sequencer keys, or fallback order routers that can be manipulated behind closed doors.

-

There are no whitelisted bots, insiders, or “preferred liquidators.” Every actor competes in the same public space under the same constraints, enforced by code, not trust.

- MEV-Resistant by Design, Not Just Policy

-

MEV resistance is embedded at the following levels:

-

Matching Logic: Transparent sequencing and batch pricing

-

Settlement Flow: Atomic execution with no opportunity for reordering

-

Liquidation Handling: Permissionless, pre-validated, and queue-based

-

Validator Rules: Tendermint BFT prohibits validator-induced reordering

-

-

The system is engineered such that extracting value via MEV is not just discouraged but it's rendered unprofitable.

- Composability Without Compromise

-

Protocols, bots, and strategy vaults can safely integrate with TradeView’s order book and execution layer without fear of being front-run or reordered.

-

This opens the door for structured products, vault automation, and arbitrage strategies, all protected under the same MEV-resistant guarantees.

TradeView doesn’t rely on assumptions of honest actors or obscure sequencing guarantees. Instead, it builds incentive alignment, execution integrity, and validator neutrality directly into the matching layer, creating an infrastructure where trust isn’t necessary, because manipulation is structurally disincentivized.

4.10.4 Integration with Tendermint BFT

TradeView’s execution environment is tightly coupled with Tendermint BFT (Byzantine Fault Tolerance), a proven consensus engine that forms the backbone of its validator set. While most DEXs struggle with either centralized sequencing (rollups) or probabilistic finality (Ethereum-style chains), TradeView leverages deterministic block production, instant finality, and validator accountability to enforce MEV-resistance directly at the consensus layer.

This is not a workaround but it’s an intentional architectural alignment between consensus and execution.

- What Makes Tendermint Ideal for MEV Defense?

-

*Deterministic Block Finality* Each block is finalized once ⅔+ of validators reach agreement — there’s no chance of reorgs, uncle blocks, or rollbacks.

→ Once an order is confirmed, it’s permanent. No room for post-hoc reordering or slot sniping. -

*No Mempool Games by Validators* Validators do not compete to include transactions for priority fees.

→ This removes the economic incentive to front-run, delay, or reorder pending orders. -

*Predefined Block Proposers* Tendermint assigns proposers in a round-robin or stake-weighted fashion, which removes random sequencing variance.

→ Bots and insiders can’t game “which validator comes next” to anticipate timing advantages. -

*Slashing for Misbehavior* Validators that deviate from consensus rules — including incorrect execution or non-deterministic outputs — are slashed.

→ This enforces protocol-level discipline and keeps MEV-style collusion in check.

- How TradeView Utilizes Tendermint for MEV Protection

-

*Deterministic Order Inclusion Rules* Every validator receives the same mempool, the same order set, and runs the exact same matching logic.

→ No validator can reorder trades for personal or third-party benefit. -

*Execution Integrity by Design* TradeView’s smart contracts are deterministic:

-

Order matching

-

Liquidation checks

-

Settlement flows

-

All yield the same result, regardless of which validator processes the transaction.

-

*Consensus-Tied Matching Engine* The matching engine is tightly embedded in the consensus runtime.

→ Orders are not executed after consensus — they are executed as part of consensus. -

*Global Synchronization for Liquidation Triggers* Because every validator sees the same state and price feeds at the same time, no validator has an advantage in triggering liquidations or reaping associated rewards.

-

*No Sequencer, No Central Relayer* Unlike rollups or hybrid chains, there is no single party deciding the order of transactions.

→ Order sequencing is governed by protocol logic and consensus rules — not by human discretion.

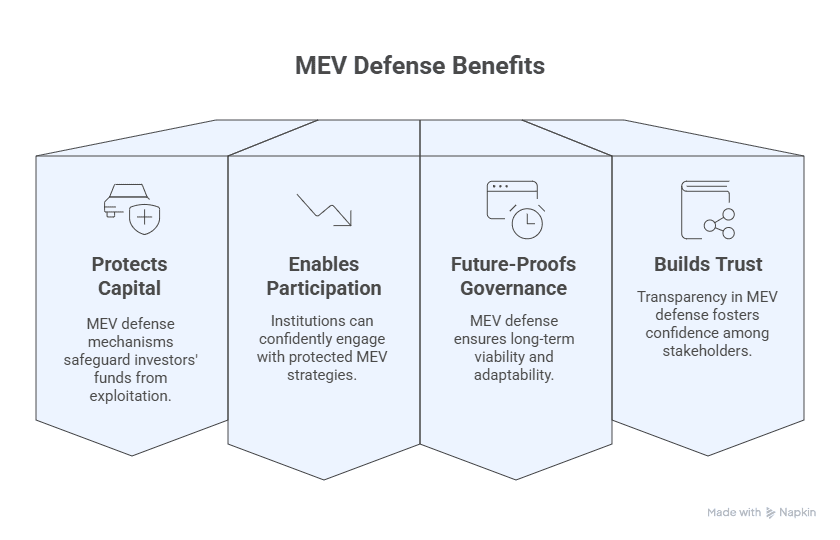

- The Investor Angle: Why This Matters

-

*Protects User Capital* Traders, especially those using leverage or strategy automation, can rely on execution integrity.

No unexpected slippage. No front-running. No tampered liquidations. -

*Enables Institutional Participation* Funds and market makers that require clear trade auditability and deterministic pricing get the infrastructure they need — without exposure to validator or bot games.

-

*Future-Proofs Governance & Compliance* The protocol can be upgraded by governance without reintroducing centralized dependencies.

No backdoors, no admin keys, no special validators with ordering privileges. -

*Builds Trust Through Transparency* TradeView’s use of Tendermint means that execution behavior can be mathematically proven and audited, not assumed.

TradeView doesn't just deploy on Tendermint. It uses Tendermint’s deterministic consensus and slashing model as a core building block of its execution fairness.

The result is a perpetual DEX that institutional traders, market makers, and power users can trust, block after block, trade after trade.

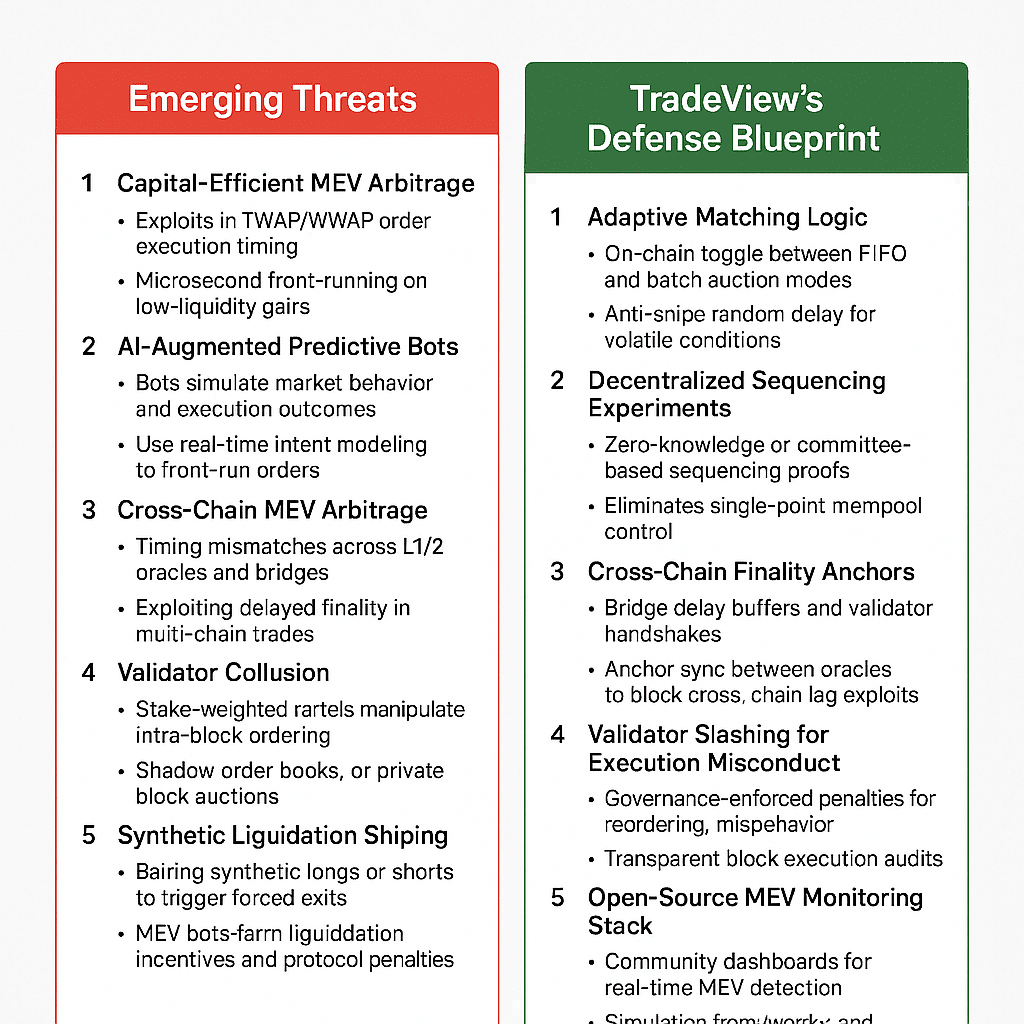

4.10.5 Future Considerations: Sustaining MEV Resistance at Scale

TradeView’s current MEV mitigation stack is robust by design — but MEV isn’t a static threat. It evolves. As the protocol grows, volumes scale, and strategies become more complex, so too will the adversaries. The challenge isn’t just neutralizing today’s MEV vectors — it’s ensuring long-term protection without sacrificing performance, composability, or decentralization.

This section outlines how TradeView will future-proof its MEV-resistance framework to stay ahead of both attackers and protocol complexity.

- Dynamic Threat Landscape: Why MEV Won’t Stand Still

-

*Capital-Efficient MEV Will Rise* As slippage and spreads tighten, even sub-second advantages will become extractable.

→ MEV bots will exploit not just price latency, but timing of funding rate flips, liquidation thresholds, and OCO triggers. -

*AI-Augmented MEV Strategies* Attackers will combine public mempool visibility with predictive ML models that simulate probable execution paths.

→ These “intelligent MEV bots” could pre-position orders or spoof intent. -

*Cross-Chain MEV Arbitrage* With collateral and liquidity bridged across multiple L1s and L2s, new arbitrage surfaces emerge:

-

Delay-sensitive trades on one chain triggering front-runs on another

-

Oracle lags used to exploit synthetic markets

-

-

*Validator Collusion Risks* As validator sets scale and incentives increase, the risk of small clusters coordinating to reorder or censor will rise — even in BFT models.

C. TradeView’s Long-Term Strategy for MEV Defense

TradeView’s MEV protection model is designed not just as a static guardrail but as a modular, upgradable security framework. Here's how it will evolve to meet future threats:

1. Adaptive Matching Logic

-

Matching contracts will support on-chain toggling between price-time priority and batch auction modes depending on volatility, order congestion, or governance choice.

-

Future upgrade: Random delay injection into sequencing to prevent gas sniping during predictable spikes (e.g., CPI data, major listings).

2. Decentralized Order Sequencing Experiments

-

TradeView will test optional decentralized mempool sorting protocols, where:

-

Validators propose order sets

-

Sequencing logic is enforced through verifiable computation

-

Community members (or zero-knowledge provers) verify that ordering rules weren’t violated

-

3. MEV Risk Scoring per Transaction

-

Future blocks may include “MEV Risk Flags” or scores attached to incoming transactions.

-